Ivory Coast-Ghana: A fairer and more sustainable cocoa sector with the DRD?

In recent years, access to a decent income for producers has become a priority for the cocoa industry, particularly in Côte d'Ivoire and Ghana, the world's two leading exporters. The governments of these countries recognized this by adopting, in October 2020, the Decent Income Differential (DRD), a premium of 400 $/tonne of cocoa sold, fully returned to producers. Three years later, have the effects been beneficial? After a reminder of the context, FARM gives the floor to Nitidae, an NGO specializing in industry development and environmental protection. Their experts are calling for a "new deal" for cocoa.

Ivory Coast-Ghana: two heavyweights of the global market

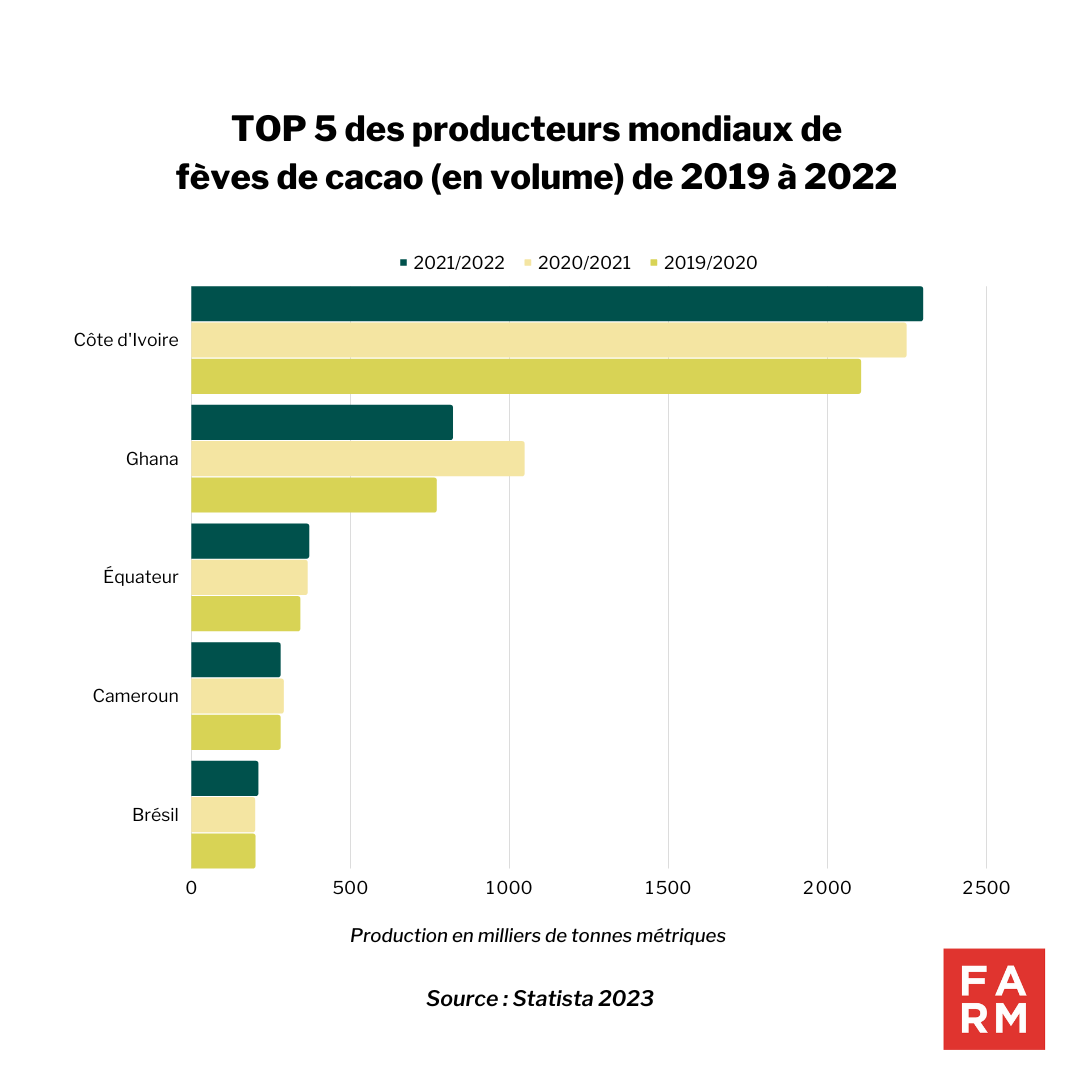

In 2022, global cocoa production was to nearly 5 million tonnes and near 80% of her came from family plantations less than 10 hectaresIvory Coast and Ghana are the leading producers and contribute more than 60,000 to the marketing of cocoa beans.

The global cocoa market is characterized by both a steady increase in volumes consumption and production (4.8 million tonnes in 2020-2021 compared to 3.6 million tonnes in 2008-2009) as well as strong variability in cocoa prices in a general downward trend (-2% per year since 1960) while the price of the chocolate bar evolves independently of this market. The increasing quantity of cocoa produced and available on the markets, combined with the fall in price has had consequences on producers' income. Most of them live elsewhere below the poverty line and most often have few alternative income-generating activities.

The global cocoa market is characterized by both a steady increase in volumes consumption and production (4.8 million tonnes in 2020-2021 compared to 3.6 million tonnes in 2008-2009) as well as strong variability in cocoa prices in a general downward trend (-2% per year since 1960) while the price of the chocolate bar evolves independently of this market. The increasing quantity of cocoa produced and available on the markets, combined with the fall in price has had consequences on producers' income. Most of them live elsewhere below the poverty line and most often have few alternative income-generating activities.

A dozen large international companies (European and American, mainly) are shared almost of 80 % of the world cocoa trading marketThe latter is a market for commodities (standardized raw materials, little or not processed and traded in large volumes) and not for “specialty” products. “Crudes” (Latin America, Madagascar) and labels (Fair, Organic) still represent a small part of global trade (less than 5% according to the NGO Max Havelaar), despite progress on European markets.

Focus – Cocoa, the brown gold of Ivory Coast

Ivory Coast-Ghana: the leading role of public authorities

In Ivory Coast and Ghana, The cocoa industry is administered by the public authorities. The latter play several roles, in particular that of controlling the access of private operators (national and international) to the different functions/professions of the sector, from purchasing field edge (directly to the farmer) to export through processing and the supply of inputs.

They also establish references on prices and margins for the links in the chain, finance expenditures of common interest and manage reserve funds allowing prices to be smoothed for producers from one year to the next.

In Ivory Coast, Exporters are private companies that have acquired export licenses from the Coffee and Cocoa Council (CCC) for a reference volume and price, before the main season (October to March). Exporters purchase cocoa directly from cooperatives or other operators approved by the CCC to cover export contracts/licenses granted by the CCC. Advance sales allow the CCC to set a price at the beginning of the season. anticipated average selling price (including cost, insurance and freight – CIF) from which a minimum farm gate collection price is defined. The objective is a farm gate price of 50 to 60 % of the CIF price.

In Ghana It is the Cocoa Marketing Company (CMC), a public entity, which receives cocoa beans from all approved purchasing companies (called LBC) through its three aggregation stores (Takoradi, Tema, Kumasi). It handles the export of beans and supplies national processors. The latter are free to export processed products. There is therefore a regulated liberalization of farm-gate purchasing and local processing.

The DRD to combat poverty among cocoa farmers

THE Living Income Differential (DRD) is a mechanism that aims to ensure that Ivorian and Ghanaian cocoa producers receive a decent income from their work. The DRD is based on the observation that the price paid to producers and set by the international market is insufficient. The DRD helps to rebalance this low price in favor of a fair price for their cocoa, which reflects the real costs of production as well as a reasonable profit margin.

This mechanism was officially launched in October 2020 by the Ivorian and Ghanaian governments, in collaboration with global chocolate companies and development organizations. They have thus introduced a premium of 400 USD/tonne (328.70 euros) of beans from the 2020-2021 campaign on all contracts. The primary objective is to end the persistent poverty of cocoa farmers and protect them against fluctuations in world prices of this brown gold.

Three years after the implementation of this system, have producers been able to benefit from a better income? We gave the Nitidae teams the floor, an NGO specializing in the development of sectors and environmental preservation, to assess the DRD.

FARM Foundation: What are the foundations (political and ideological) and principles of DRD?

Nitidae : To talk about the Decent Income Differential (DRD), it is important to understand its context. The announcement of this mechanism in September 2019, and its implementation in 2020, comes in a particular context both at the level of Côte d'Ivoire and Ghana and at the level of their relations with the European Union.

Since 2018, the two countries have been negotiating, with the support of the World Bank, the establishment of a partnership to better align their policies for regulating the domestic and foreign marketing of cocoa.[1]. Until now, they have often played on competition rather than complementarity.[2]. Lthe 2018/2019 campaign[3] was marked by relatively low prices (750 FCFA/kg in Ivory Coast, 7.6 Cedis/kg in Ghana) and the two regulatory institutions (CCC And COCOBOD) are in a delicate financial situation which does not allow them to support purchase prices from producers and world prices remain desperately low. Room for maneuver is therefore very limited while The purchase price of cocoa influences the income of a huge part of the rural population. The two countries therefore decided to play an unexpected card: force the international market to rise by forcing cocoa buyers to pay a premium of 400 USD/t (+/-18% of the value at the start of Ivorian and Ghanaian ports in September 2019) to be able to access their beans.

From March to June 2020, the COVID crisis caused a further drop in world cocoa prices, for both governments it is therefore necessary to act and the budgetary room for maneuver being extremely reduced (it is also necessary to finance emergency aid to the populations and the measures to fight the epidemic), only the regulatory tool is available. It is in this context that the two regulatory bodies impose in July 2020, the payment of this premium on all advance sale contracts of the harvest which will start in October 2020, just before the elections.

The idea is inspired by the model of "certified" beans, practiced in niche markets (organic, label, fair trade), which provides for premiums paid to producers with an impact on consumers via the final price. The idea was to apply this model to the entire production scale in a market where a large part of the added value is generated downstream. Indeed, the "branding", "packaging" and "marketing" of chocolate absorbs on average around 30 % of the final value of a chocolate bar and rises to more than 50 % for a Kinder© egg). The downstream sector could therefore absorb a large part of this premium without it being fully passed on to consumers.

This “imposed” bonus seems all the more justified since 30 to 40 % of the production of the two countries already has a "sustainable label" (UTZ certification, Rainforest Alliance or internal labels of most major chocolate makers). In addition, the European Union published a communication in July 2019 announcing that it is working on a regulation against deforestation linked to its imports[4]Since all production must become sustainable in the sense of preserving tropical forests, it was necessary to include the income of producers (and the GDP of producing countries) in the upcoming negotiations.

And it is completely logical and justified! The driving force behind the DRD could therefore be summed up as follows: "You want us to better control the negative environmental externalities of our production, so pay for it! In addition, we will ensure that a portion of this revenue goes directly to producers."

FARM Foundation: Did the DRD work as advertised?

Nitidae : Unfortunately, it can be said that the DRD did not work. As shown researcher François RUF which confirms our continuous monitoring of the market within the framework of the N'kalô service, producers did not benefit from the expected price increase, and during the 2020/2021 campaign, they even lost income due to the confusing implementation of the system.

From our point of view, there was onlyonly one real positive point of the DRD : subtracting 400 USD/t[5] to the collection systems (taxes and compulsory levies) of the CCC and COCOBOD, The DRD had the direct effect of reducing taxes on cocoa exports. It is therefore in some way a tax transfer from the State to the producers and, concretely, it corresponds to an increase of between 4 and 8 % in the producers' income.

The problem with the DRD stems mainly from poor consideration of the functioning of the downstream part of the cocoa industry.. It assumes that the branding/packaging/marketing costs of chocolatiers are easily reducible. This is not true. Selling chocolate generally means selling confectionery at a price significantly higher than that of most other confectionery.

We're not talking about a small deviation... just take a look at a supermarket website, MDD chocolate (editor’s note: private label) costs between €10 and €25/kg, while sugar-based confectionery costs between €4 and €8/kg. To convince consumers, you have to invest in marketing, even in countries where chocolate is well established in consumer habits. So, when prices rise, all chocolatiers reduce the size of the bars (this can go down to 75g instead of 100g).

Then, we assume that big brands, sensitive to their image, will "make an effort" if we accuse them of not paying the right price. But cocoa buyers are not chocolate brands known to consumers! More than 75 % of beans are purchased by grinders, the latter then sell them to hundreds, if not thousands of large, medium and small chocolate companies, but also to biscuit factories, confectioners, restaurateurs, pastry chefs, etc.

Certainly, there is a concentration of players in the cocoa sector at the grinder level – the 10 largest companies carry out 80 % of global grinding – but the latter are intermediaries, subject to competition from a multitude of customers who work in a multitude of markets and for whom the price of the key ingredient (cocoa) is a strong determinant of production costs and margins.

The technological context has made cocoa an ultra-processed product. The industrialists involved in grinding and transforming butter (the "butter makers") market "ready-to-use" cocoa-based products for manufacturers (or brands) known to the general public, whether industrial or artisanal. The majority of them therefore have no direct business links with producers (or their organisations), which accentuates the dilution of responsibilities in defining and implementing a "fair price".

Finally, regulating agricultural markets in the long term by coercion alone (law, regulation and/or penalties) does not work or works little, especially on the scale of international trade. Within the European Union, we can think of the famous butter mountains from the early 80s, or to the International Coffee Agreements which have never succeeded in stabilizing the market. The law of supply and demand always and tirelessly takes over. An operator who is smarter than the others or better informed will systematically find a way to circumvent the device and the others will follow suit.

FARM Foundation: In 2023, we saw an increase in the price of cocoa on the international market. Why?

Nitidae : Indeed, the 2022/2023 campaign is the only one where the DRD mechanism has had any semblance of effectiveness. The governments of Côte d'Ivoire and Ghana have forced the largest grinding companies and major chocolate makers to sign an agreement in which they committed to respecting the initial principle of the DRD, namely payment of the international market price in addition to the premium. And not the international market price, including premium, as was the case in previous campaigns.

This campaign is taking place in a context of relative stability, or even a slight decline, in global production. As a result, other producing countries have more readily aligned themselves with the conditions proposed by Côte d'Ivoire and Ghana.

This raises an interesting point: in times of undersupply, states or regulatory bodies can potentially "accelerate" the rise in producer prices by regulating contracting conditions. But this unfortunately does not address the main problem: how do we protect producers against price drops?

FARM Foundation: In your opinion, what public policies could truly ensure the objectives of the DRD, namely stabilizing world cocoa prices at a higher average level than during the 2000s and 2010s?

Nitidae : In the history of agricultural policies, and in particular in that of perennial crops, there is at least one tool (available in different forms) which has proven itself in terms of combating overproduction and falling prices. This concerns the regulation of supply, and in particular grubbing-up premiums. (or renewal/conversion). It is an expensive tool but it is certainly effective. There are many examples of success, both in Europe, particularly in the vineyard or in certain tree-growing sectors, and in Asia in the rubber and palm oil sectors.

In the context of Côte d'Ivoire and Ghana, such a policy could have a strong social impact. Among cocoa producers, those who are generally the most vulnerable are the owners of aging plantations. Their yields are falling year after year, their income too and they suffer a real downgrading. It is extremely difficult for small family farms to give up part of their income to replant trees which will only generate income equivalent to current income after 5, 6 or even 7 years.

Help these producers to cut down their old cocoa trees, either to replant new ones or to plant something else (food crops, rubber, oil palm) and diversify their farms would probably be the best way to regulate supply and help the most precarious producers.

We have already made calculations and proposals on this subject, we are talking about a cost in the tens of millions of euros per year. It is not nothing, but It is clearly feasible on the scale of both countries. It would then be necessary a real commitment from the governments of producing countries, the private sector and technical and financial partners, starting with the European Union, whose ambition is the sustainability of the cocoa sector. Considering the amounts usually devoted to public development aid and to the sustainability programs of private operators, such an ambitious program of supply regulation is realistic. It would be a kind of Cocoa “New Deal”.

FARM Foundation: The DRD aims to improve the economic sustainability of cocoa cultivation. What about the social and environmental sustainability of production methods in the sector, particularly to address the challenge of combating deforestation?

Nitidae : Today, the "sustainability" programs of the majority of chocolate makers are centered on the level of use of mineral fertilizers and phytosanitary treatments. Any actions on these two elements actually increase production costs and therefore have an impact on producers' income. The latter assume all the risks and this does not solve any problems in the long term: the tree ages and weakens year after year, the producer's capital depreciates.

On the issue of deforestation, the priority is first to protect the remaining forests, relaunch forestry sectors to increase tree planting and reduce pressure on the remaining trees.In the coming years, deforestation linked to cocoa is likely to be concentrated in Liberia, Sierra Leone, Ecuador and, to a lesser extent, Central Africa. Instead of deforestation, we could definitely intensify logging premium policies by prioritizing agroforestry on plots with high potential. Fallowing and forestry production on old cocoa trees would also reduce land pressure on the last primary forests. There are many possibilities, such as the "tree bonus," a payment system for "environmental services" that we tested with a chocolate maker on the outskirts of the Mabi-Yaya reserve in eastern Côte d'Ivoire.

Finally, on the social sustainability of cocoa production, the main issue is clearly improving the health system. Even child labor is directly linked to it because accidents and illnesses that immobilize one or more workers are one of the main factors in school dropouts. On this point, it is a broader public policy which will require the establishment of a accident insurance and then social security for cocoa farmers.

[1] Both countries strictly regulate domestic marketing and stabilize national prices by relying on early, partial and staggered sales of their production.

[2] Ghana holds a grudge against Ivory Coast for having overtaken it in terms of production in the late 1970s and for having succeeded in developing the world's largest processing industry; Ivory Coast is unhappy that Ghana (which taxes its cocoa exports less) smuggles in and exports part of its production in certain years. For a more historical analysis, and in particular the institutional aspect: https://www.cairn.info/revue-internationale-des-etudes-du-developpement-2020-3-page-199.htm?ref=doi

[3] Cocoa marketing campaigns officially begin in October (the main harvest generally begins between late August and mid-September)

[4] https://commission.europa.eu/publications/eu-communication-2019-stepping-eu-action-protect-and-restore-worlds-forests_en

[5] One of the principles of the creation of the DRD is that the premium of 400 USD/t must be directly paid to the producers, so that it is removed from the tax base for cocoa exports.