Wheat and war in Ukraine: what impact on Africa?

As the Russo-Ukrainian conflict drags on, wheat supplies to African countries that rely on foreign sources are a major source of concern. This supply is primarily dependent on the export capabilities of the European Union and Russia, and the reduction in Ukrainian wheat supplies further reinforces dependence on these two major players. Three unknowns will weigh heavily on the future: the hypothetical renewal of the Black Sea corridor, global grain logistics and possible weather accidents.

Of the 200 million tonnes (MT) of wheat available on the world market, 13 million tonnes are imported each year by sub-Saharan African countries. These volumes are distributed across a large number of countries, thus placing sub-Saharan Africa in a situation of less dependence than North Africa (15 %) and the Middle East (16 %), They are also major importers of wheat.

Black Sea Maritime Corridor: Where is Ukrainian Wheat Going?

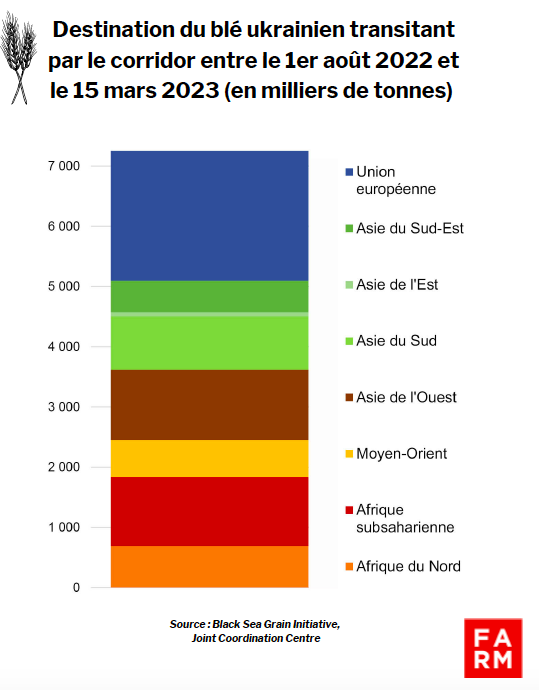

By mid-March 2023, one year after the start of the war in Ukraine, more than 800 ships passed through the Black Sea corridor, allowing the flow 7.3 MT of wheat since 1er August 2022Half of these volumes went to Africa, the Middle East and Turkey, 30 % to the European Union, while the rest was destined for South and Southeast Asia.

(Reading: West Asia includes Turkey exclusively; South Asia includes Sri Lanka, Bangladesh and Afghanistan.)

Since the Black Sea Corridor began operating, Ukrainian wheat was gradually able to regain its pre-war markets, but in still very small volumes.. Over the eight months of operation of the corridor, barely 800,000 tonnes of wheat were shipped to North Africa from Ukraine compared to 5 to 6 million tonnes on average during previous campaigns. To the Horn of Africa, 1 MT was shipped, partly via the World Food Programme in response to the security and climate crisis facing the region. In addition, 300,000 tons were sent to Yemen and Afghanistan, two warring countries heavily dependent on food aid. Finally, 1.2 MT was purchased by Turkey, a country that is a hub as a major wheat processor and the world's largest flour exporter.

The European Union is now the first destination of Ukrainian wheat, by sea and land, whereas it was only a minority, or even negligible, destination before. This new situation reflects Ukraine's attachment to European logistics networks due to the rise in solidarity corridors, or Solidarity lanes, set up with the support of the European Union. Ukrainian wheat came in part to supply a European market in fodder deficit following the drought that affected the corn harvest last summer. However, the fate of the significant volumes imported by the European Union is questionable.

The European Union, a new platform for re-exporting Ukrainian wheat?

The Russian-Ukrainian conflict has revealed the strategic importance of two European Union trade routesThe first to the south, from the ports of Constanta (Romania) and Varna (Bulgaria) on the Black Sea. The second to the north, from the ports of Poland and the Baltic States on the Baltic Sea. The first route mainly serves North Africa, while the second mainly reaches sub-Saharan Africa. These trade routes have emerged over the last ten years thanks to the growth in cereal production in these Central European countries, which have, in fact, increased their exports. Between 2011 and 2022, the share of these sources in the European Union's wheat exports to Africa increased from less than 5 % to almost 50 %.

These trade routes are being mobilized to re-export Ukrainian wheat following the rise of the Solidarity lanes. Between March and December 2022, European Union exports to Africa increased by 31.1%.[1]. This increase was partly borne by the Central European countries mentioned above (+1.6 MT compared to the same period last year), but especially by France (+3.5 MT), whose good harvest, combined with the absence of Ukrainian supply, enabled a strong return to African markets, particularly in North Africa. While the European export routes of the Black Sea and the Baltic have certainly allowed the re-export of some Ukrainian wheat, their loading capacity remains limited.

These Central European countries are nevertheless facing a double challenge : export their own production at the same time as Ukrainian volumes. These trade routes would be even more mobilized if the corridor agreement were to end, raising numerous challenges for the sectors and their producers in terms of logistical capacity, traceability, and even competitiveness. But it is more broadly in Brussels that the support that the European Union will provide for the development of these trade routes will be decided.

Supplying Africa: an equation with several unknowns

If the conflict and logistical difficulties reduce the availability of Ukrainian wheat supply at the global level, African countries depend primarily on the European Union and Russia for their supplies. These two exporters supplied 67 billion tonnes of wheat (including flour) imported by the African continent during the 2019/20 marketing year.[2]. Ukraine was the third largest supplier to the continent over the same period, with 15 % of the volumes supplied, or 8 million tonnes. The United States and Canada follow, together accounting for 11 million tonnes of delivered volumes. A few countries provide a "top-up" supply with occasional, more modest volumes. These are Argentina, Australia, India and Turkey (mainly flour).

Since the start of the war in Ukraine, European exports to Africa have increased significantly, while those from Ukraine have declined significantly. A few minority suppliers, such as Argentina, Brazil, and Australia, have been able to export additional volumes. However, in the absence of Russian export data, it is difficult to have an overall picture of Africa's supply in recent months. Yet, given its record harvest, Russia will be more than ever a decisive player in the wheat market this year. This is evidenced by numerous diplomatic exchanges, such as the one held between Russia and Egypt, aimed at securing supplies.

In the coming months, Africa's wheat supply will therefore depend above all on the ability of the European Union and Russia to supply the various markets. The question of sufficient supply in volume is a serious issue for North Africa, a large consumer of foreign wheat., but it is not yet in question. The consequences in sub-Saharan Africa are more heterogeneous and concentrated in the Horn of Africa. This is partly explained by the fact that the World Food Programme (WFP) has historically sourced its wheat from Ukraine.

Outside of this particular situation, we can consider that food security in sub-Saharan Africa is more impacted by price shocks accentuated by the Russo-Ukrainian conflict than by the volumes produced or exported from the Black Sea. Indeed, the conflict, by helping to keep food commodity prices high on world markets, is primarily contributing to increasing the food bills of countries dependent on imports. These imports feed a predominantly urban population, which has been facing high food inflation for three years now.

As it is, three major unknowns persistThe first and most pressing is the renewal of the Black Sea corridor on May 19th. The second will be the logistical capacity of the global market to supply countries dependent on imports, while a record harvest is expected in July, particularly in Russia. But the major unknown remains above all climatic, while global available stock levels are tightening. Global grain markets remain dependent on climatic hazards, which can weigh heavily on availability. The case of Argentina is a worrying illustration of this, as the severe drought the country is experiencing will deprive the global market of 11 MT of wheat this year.[3].

[1] According to Eurostat, foreign trade data.

[2] Calculations based on UN Comtrade

[3] Based on USDA estimates as of March 2023

3 commentaires sur “Blé et guerre en Ukraine : quels impacts pour l’Afrique ?”

Leave a Reply

You must be logged in to post a comment.

A very restrictive article that ignores Africa's resilience in dealing with the shocks caused by the crisis in Ukraine. As one of my trainers says, "Every situation is an opportunity," and you have no idea how Africa is taking advantage of this situation...

Good morning,

The focus of this article is on the specific case of wheat in order to understand the impacts in terms of prices and volumes that a potential reduction in Ukrainian supply would have on African markets. The article is not intended to shed light on how the continent ensures its food security. However, it refers to a policy brief that we invite you to consult and which addresses these topics, in particular the resilience strategies developed by producers in the face of crises: https://fondation-farm.org/etude-hausse-prix-agricultures-africaines/