Removal of Chinese customs duties: what opportunities for North African agricultural exports?

In contrast to U.S. protectionist trends, China has recently taken a major step toward opening its market to African exports. At the China–Africa Economic and Trade Expo in June 2025, Beijing announced the complete removal of tariffson imports from 53 African countries. In practical terms, this landmark measure extends duty-free access to the Chinese market to almost all African countries—a privilege previously reserved only for the continent’s least developed countries. For North Africa, this tariff opening represents an opportunity to diversify its agricultural exports to a market of 1.4 billion consumers. As part of our ongoing series on African agricultural exports, this installment examines trade relations between China and the countries of North Africa.

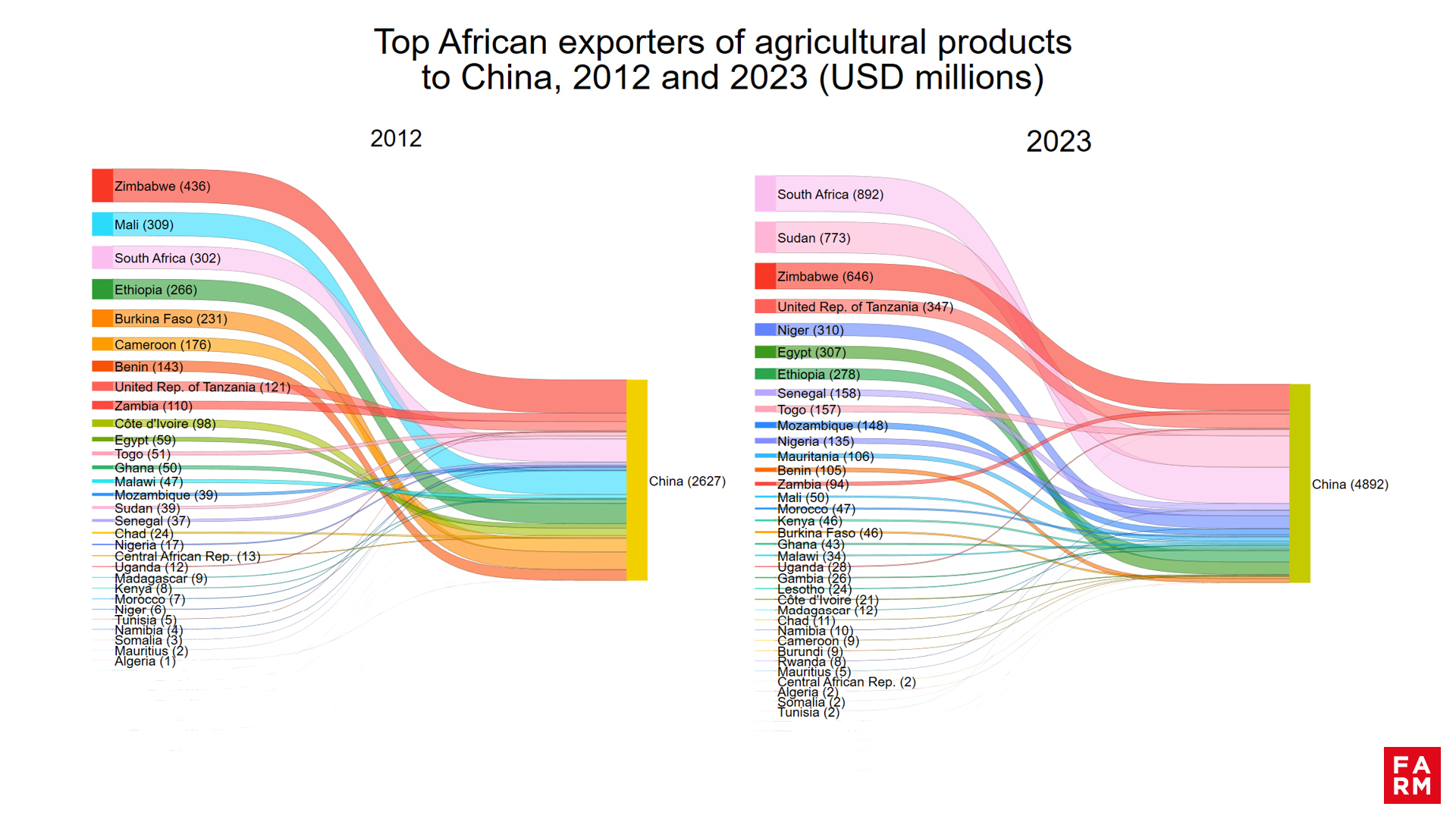

African agricultural exports to China up 86 % and North Africa's share remains limited

The continental panorama highlights a increase of 86 % of African exports to China between 2012 and 2023. The increase is driven by Southern and Eastern Africa, with major contributions from South Africa, Sudan, Zimbabwe and Tanzania. North Africa, although increasing, remains a modest contributor and accounts for around 7 % of the total export value in 2023.

North Africa: fivefold export growth in 10 years and progressive upgrading

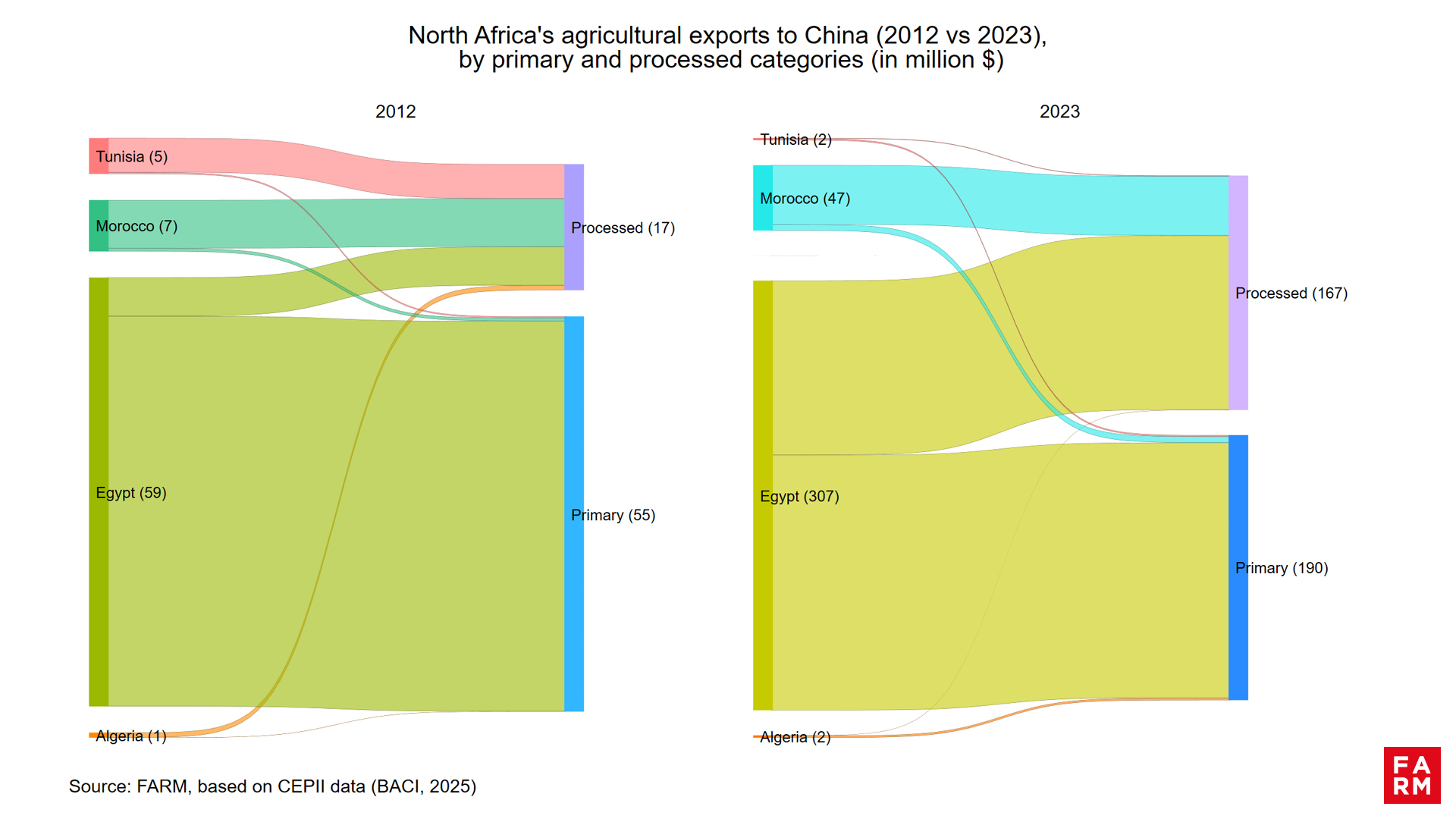

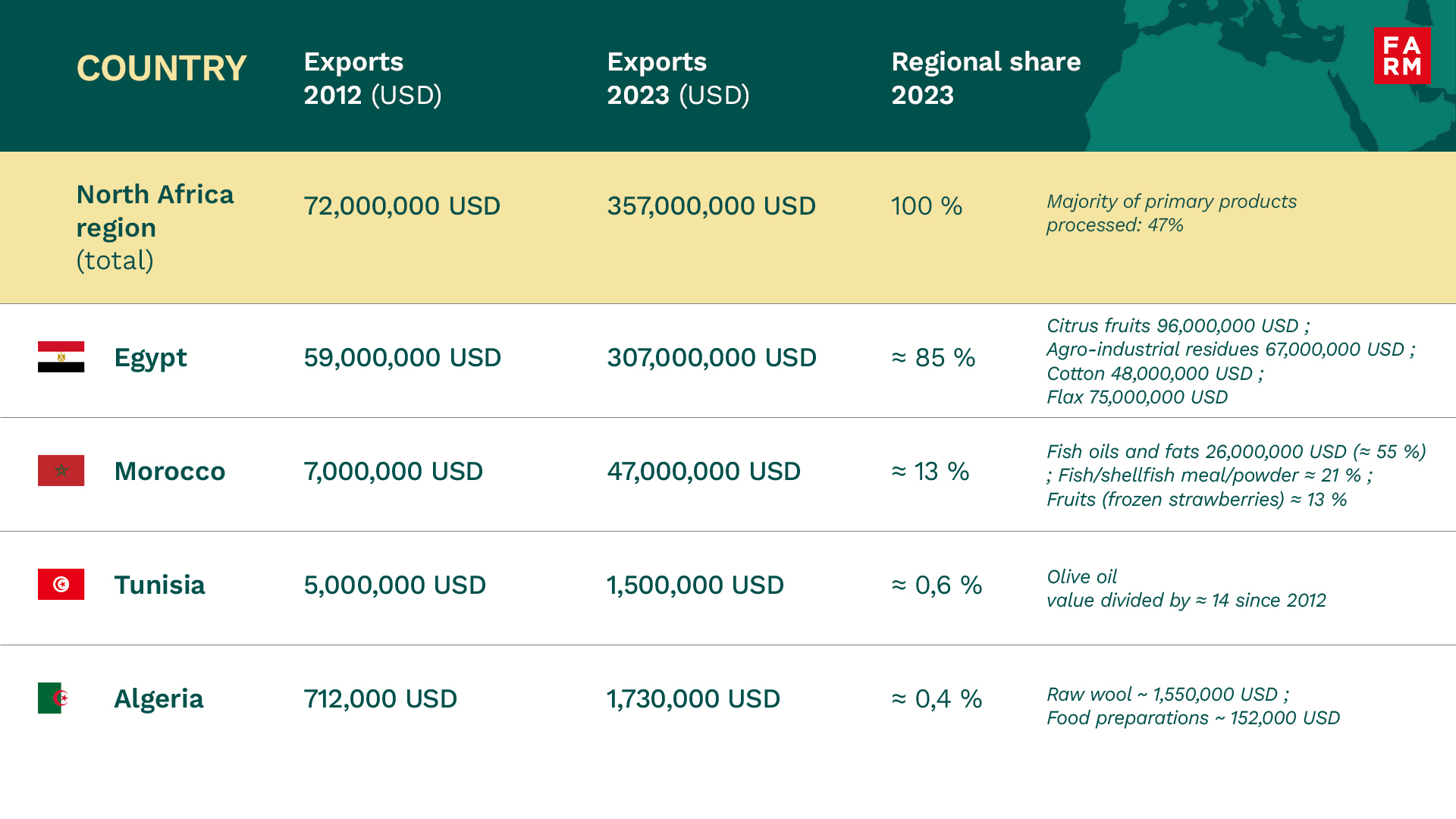

North African agricultural exports to China have grown from USD 72 million in 2012 to USD 357 million in 2023. This dynamic makes China an increasingly important trading partner for the region, even if the flows remain modest, compared to exports to Europe or the Middle East This growth is primarily based on Egypt, which represents more than 85 % of regional exports to China in 2023. Morocco has seen its exports grow rapidly (+571 %) in a decade while Tunisia and Algeria have little weight in these exchanges, with respectively 0.6 % and 0.4 % of the region's exports.

The evolution of flows highlights a qualitative transformation of agricultural exports to China. 2012, they were dominated by the primary products (76 %) while in 2023, their share has reduced and processed products represent almost half of the flows (47 %).

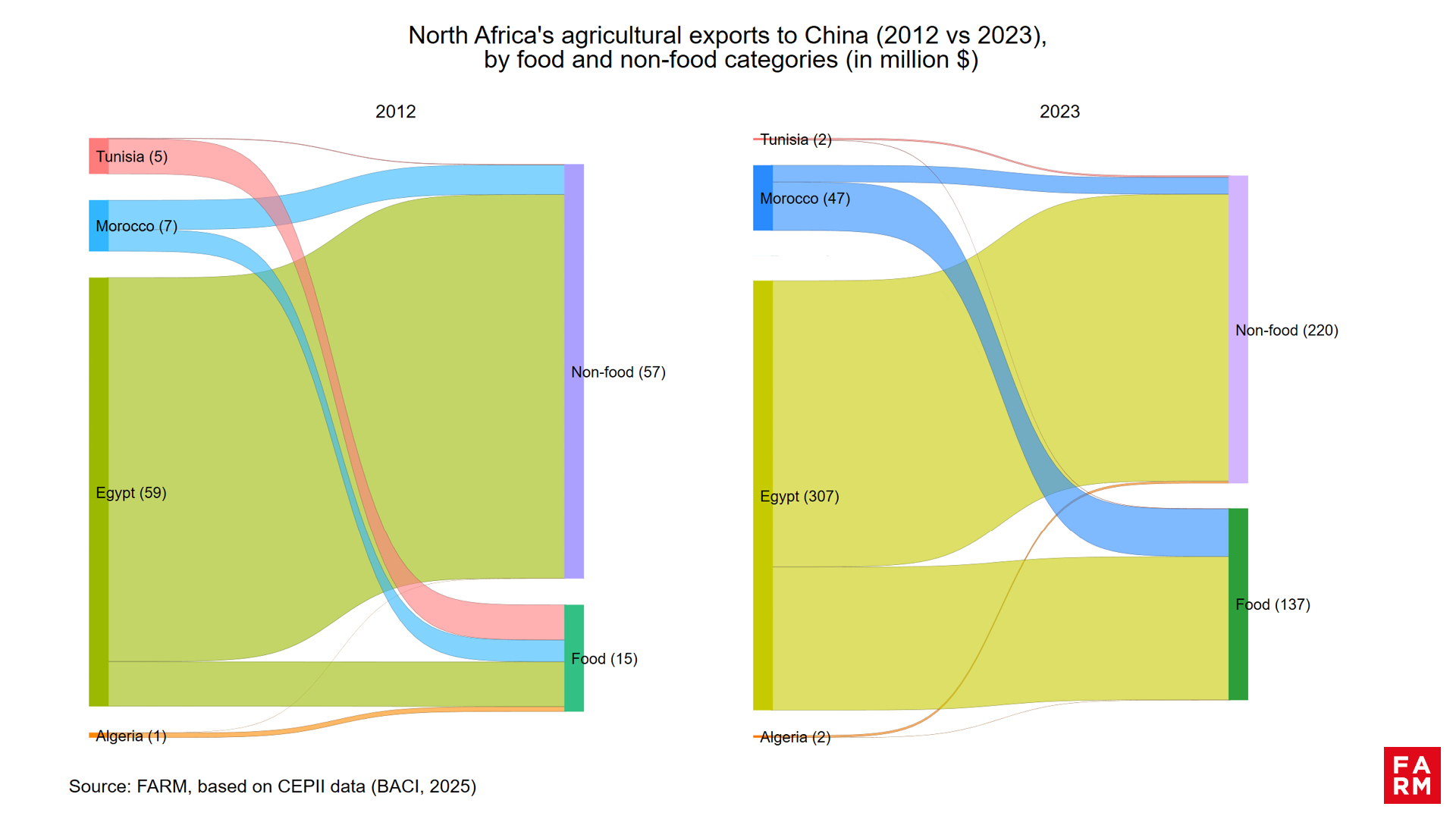

The share of food products also experienced a positive evolution over the decade, increasing from 21 % in 2012 to 38 % of agricultural exports to China in 2023. This growth is driven in particular by Egypt and Morocco, with a notable decline from Tunisia and an Algerian supply which remains marginal.

Graph 1

This progression reflects three evolutions :

- An expansion of Chinese demand beyond traditional raw materials (cotton, wool, textile fibers).

- A gradual adaptation of the North African offer to the expectations of an expanding urban market, interested in more processed food products.

- Potential for increased added value for North African sectors, which still remains largely to be exploited, as we have highlighted in previous publications.

Graph 2

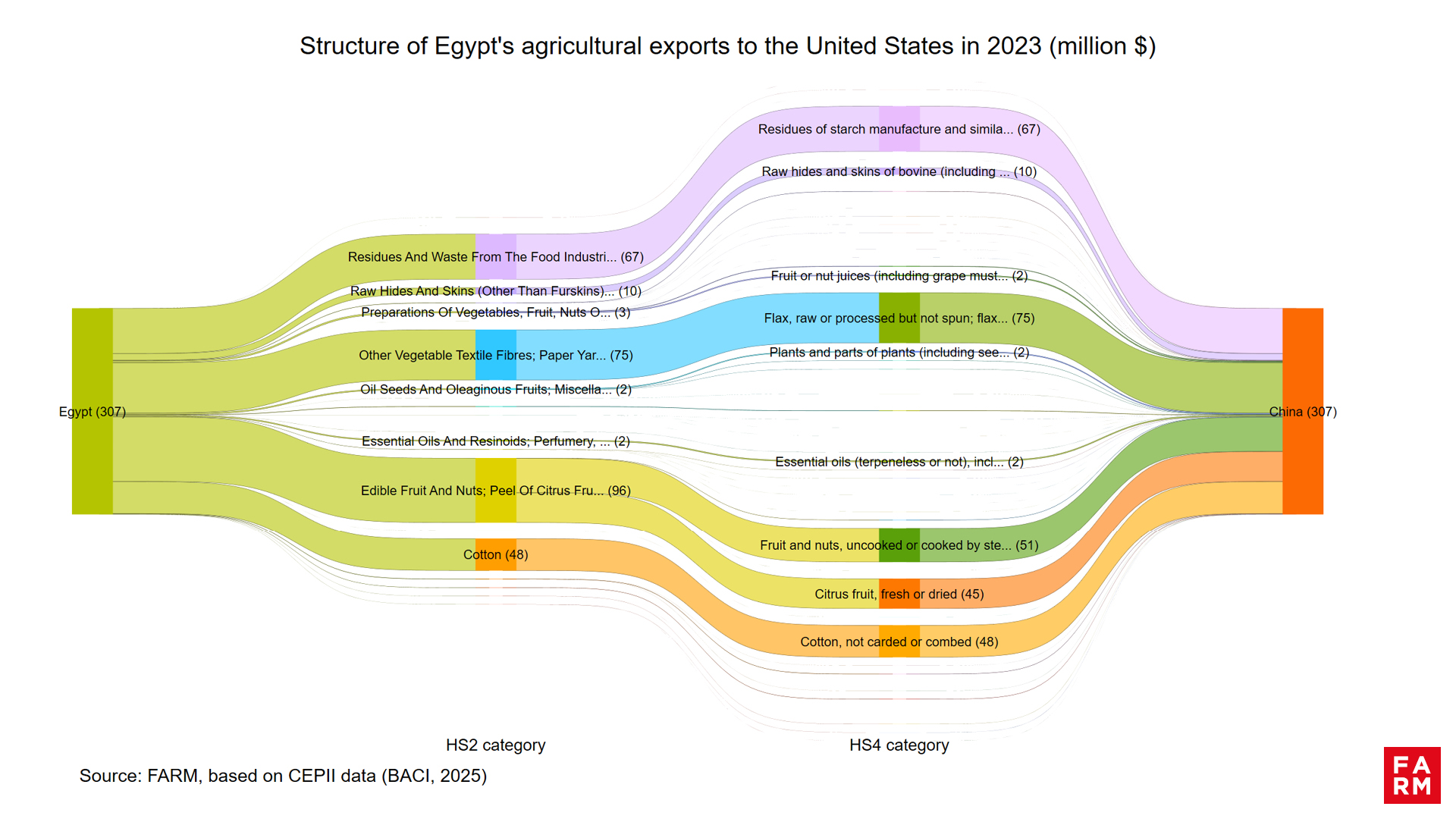

Egypt: Diversification and Regional Leadership

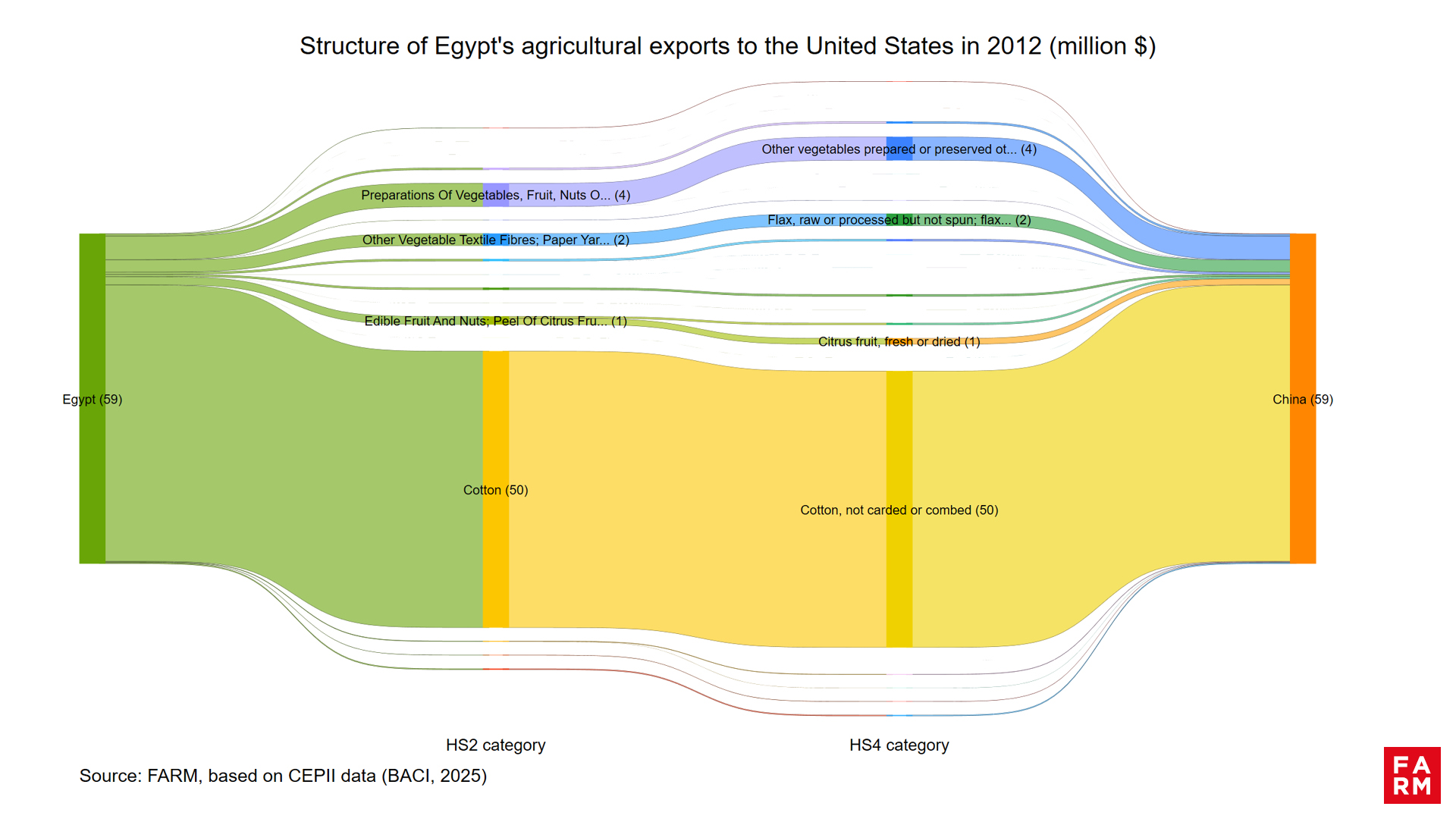

In 2012, Egyptian agricultural exports to China reached 59 million USD, relying almost exclusively on the cotton (50 million USD). Alongside this dominant product, only a few marginal flows appeared: vegetable preparations (4 million), other textile fibers (2 million) and citrus fruits (1 million). The export structure reflected a specialization in a traditional raw material, without real diversification.

In 2023, the Egyptian export profile has undergone a profound transformation, with a total value increased to 307 million USD (+ 420 % in ten years). This growth is based on a strong diversification exported products:

- Citrus and fruits : USD 96 million, including USD 51 million of frozen strawberries and USD 42 million of oranges.

- Agro-industrial residues and by-products : USD 67 million (including starch residues and other similar residues).

- Textile fibers (cotton, the amount of exports of which remained almost the same, 48 million USD, and linen 75 million USD).

This development reflects a dual strategy: maintaining market share in textile fibers while expanding the offering to food and processed products. Egypt is thus asserting itself as the leading North African supplier of agricultural products to China, concentrating more than 85 % of regional flows. The elimination of customs duties further strengthens the strategic position of its sectors, which now appear well placed to take advantage of the potential of the Chinese market.

Graph 3

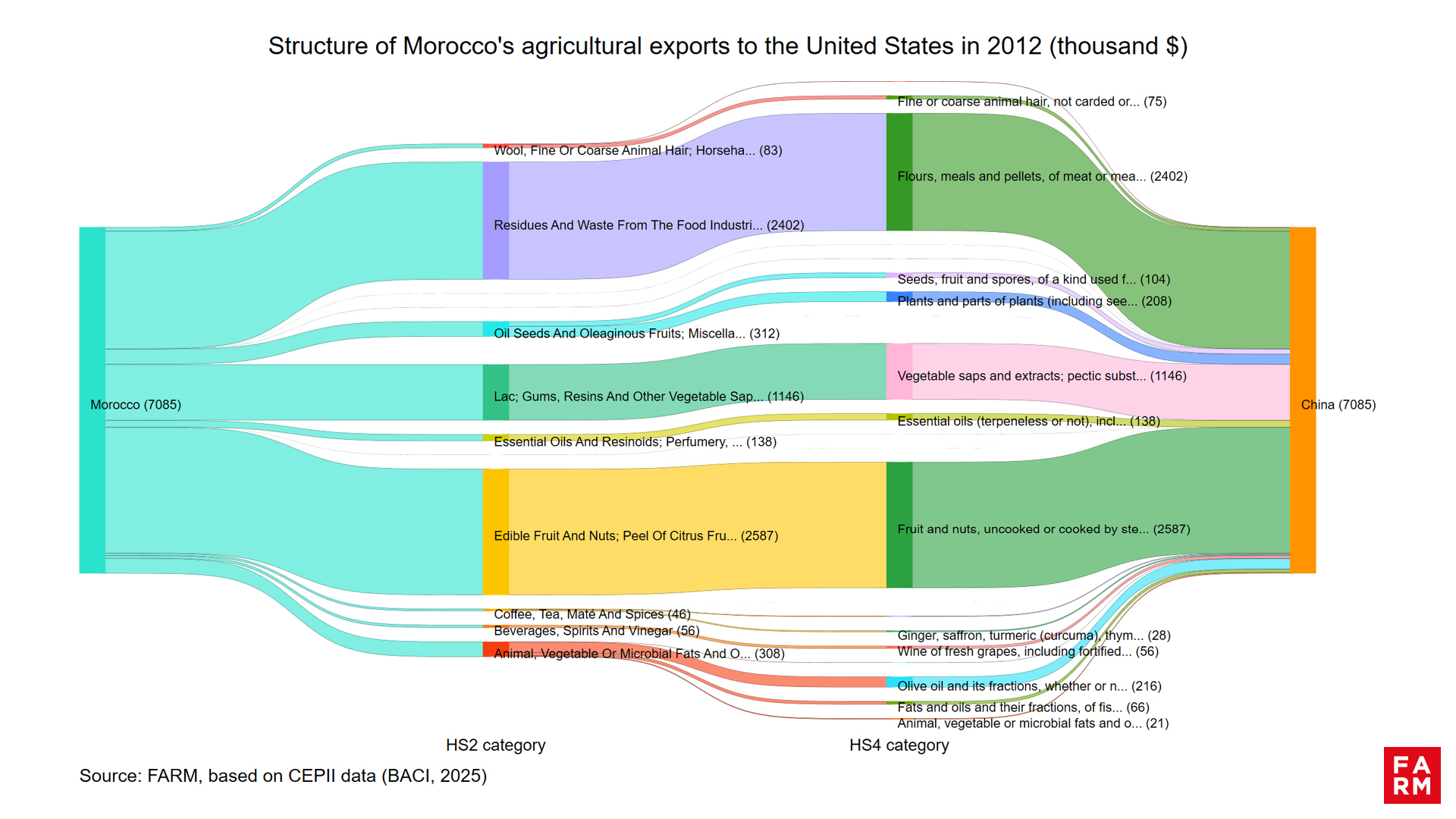

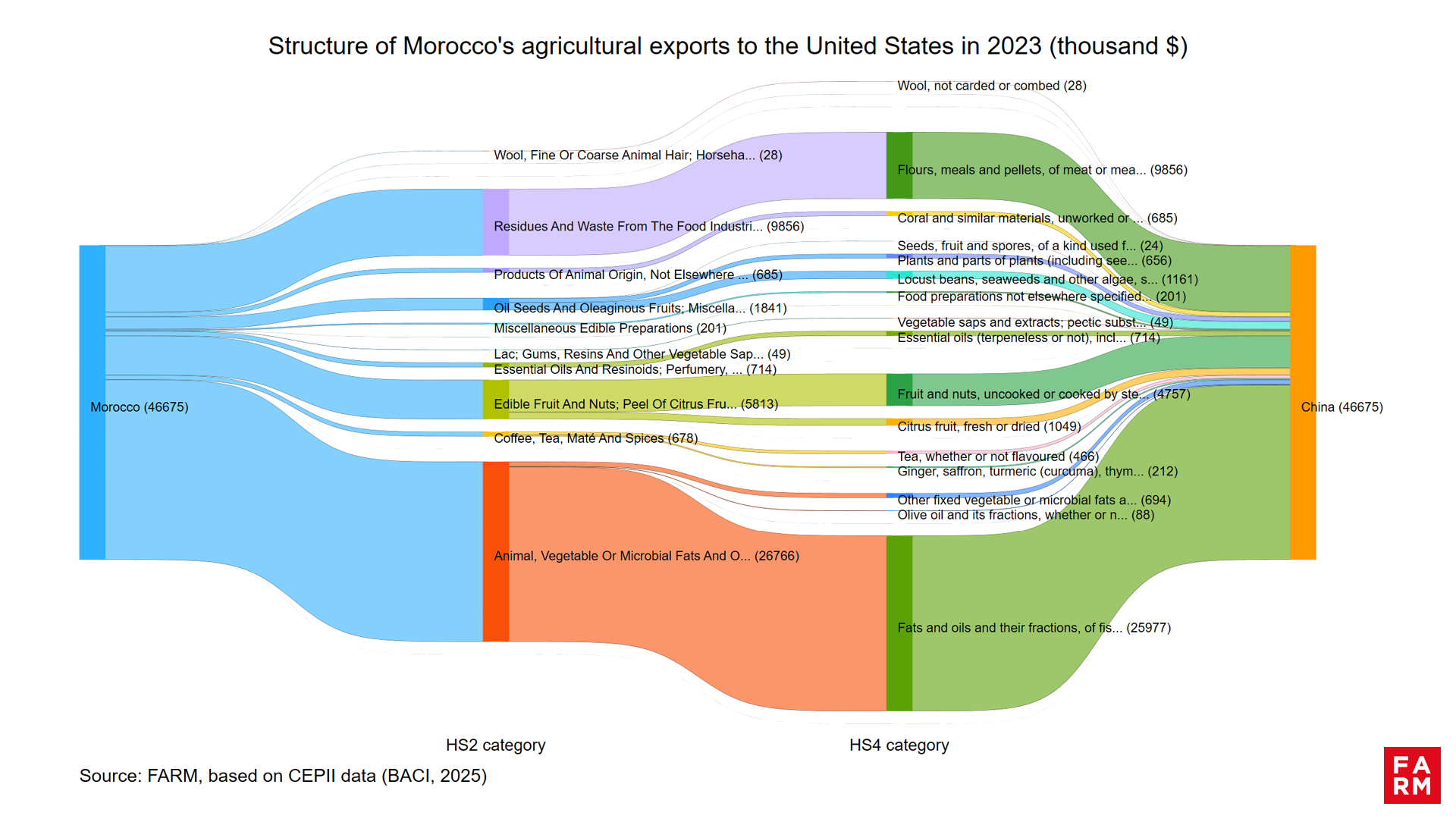

Morocco : a rising player in niche segments

Moroccan agricultural exports to China have seen a notable increase, going from 7 million USD in 2012 to nearly 47 million USD in 2023.Even if the volumes, around 13,100 tonnes of regional exports, remain modest compared to those of Egypt, the trend reflects a growing insertion of Morocco in this market.

In 2012, the flows were mainly based on a few raw products: edible fruits, including frozen strawberries (USD 2.5 million); agro-industrial residues and waste, in particular fish or shellfish flours and powders (USD 2.4 million); and vegetable gums and resins (1.1 million USD).

In 2023 , the export structure shifted and diversified, with fish oils and fats (and their fractions) becoming the leading category at nearly USD 26 million—over 55% of exports. Exports of fish or crustacean flour and powder account for roughly 21%, up +308% compared with 2012. Edible fruits remain significant at nearly 13% of export value to China, 83% of which are frozen strawberries.

This development reveals Morocco's positioning on load-bearing niches in China, in connection with changes in consumption and the gradual shift from mainly primary (resins, gums, citrus fruits) towards a presence of processed products with higher added value.

Compared to Egypt, Morocco remains a secondary player, but it is gaining in commercial visibility and has significant room for improvement. The elimination of customs duties could accentuate this dynamic, particularly for fruits rouges, les huiles et graisses de poissons, où la demande chinoise est en croissance.

Graph 4

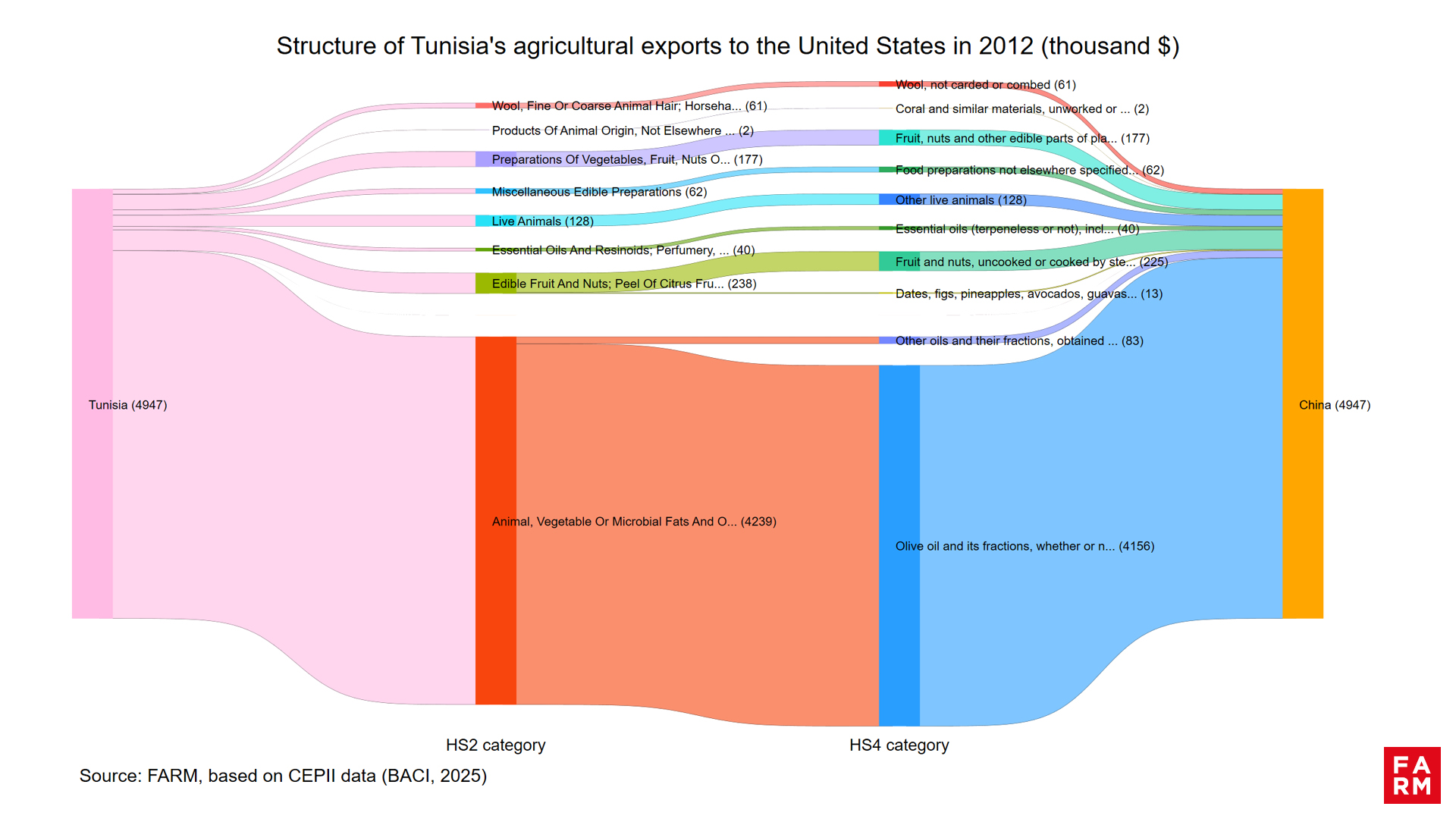

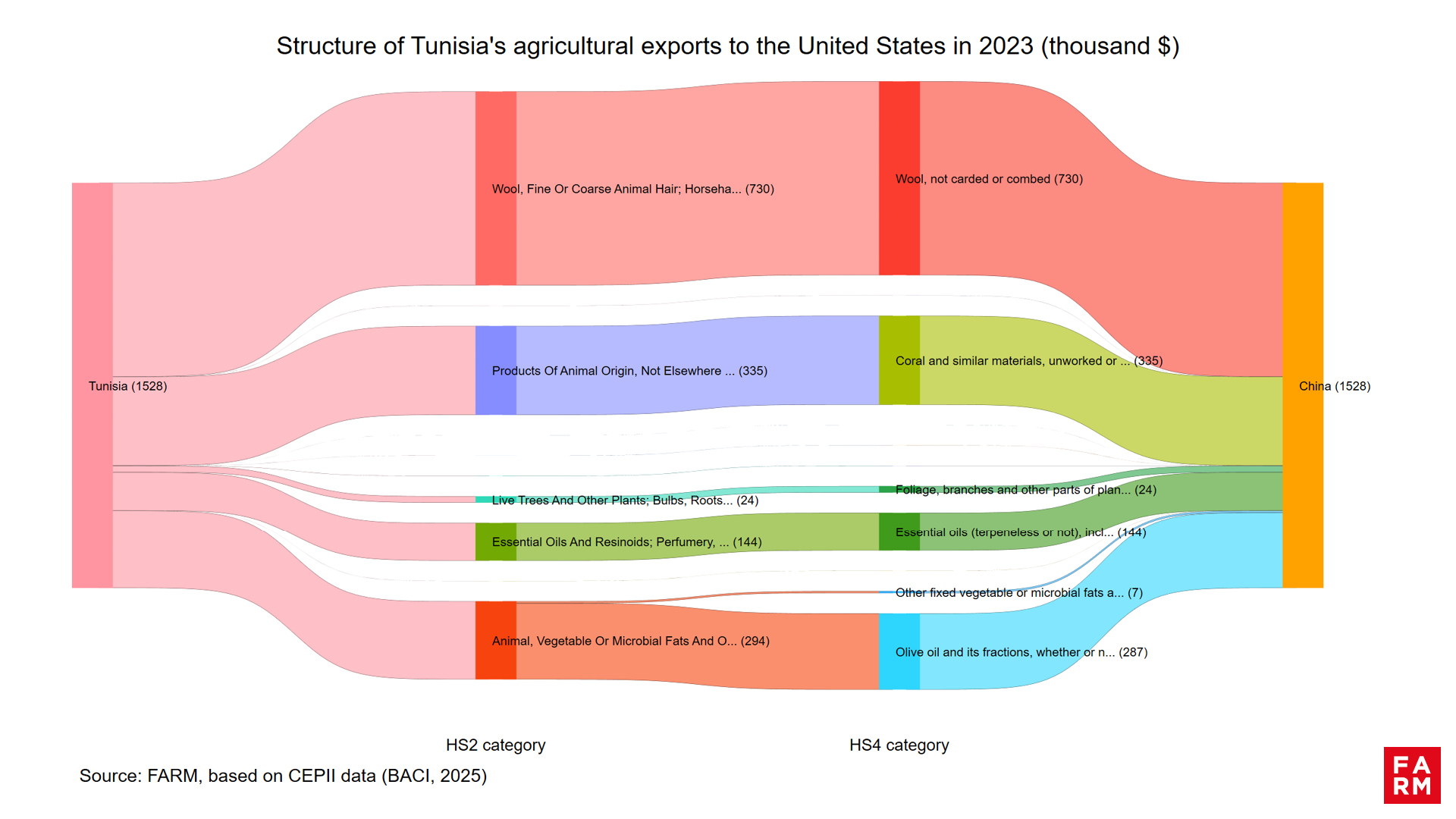

Tunisia: a marked decline in olive oil

Tunisian exports to China have increased from 5 to 1.5 million USD between 2012 and 2023This period is marked by the collapse of olive oil, the value of which has been divided by almost 14 in ten years. This decline is not so much linked to a lack of potential as to a weakness of strategic positioning in China. It can be explained by a loss of competitiveness in the face of competition from other Mediterranean players, as well as by the priority given to other markets, particularly the European Union and the United States.

China’s olive oil market is dominated by Spain and Italy—global leaders with more aggressive commercial strategies and stronger brand recognition. Tunisian olive oil is often imported in bulk and repackaged by these countries before being re-exported, which limits the visibility of the Tunisian label in this market.

The decline of the American market reinforces the urgency for Tunisia to reposition itself on other markets such as China, where a strategic opportunity for redeployment is opening up, provided that it focuses on the differentiation and promotion of its olive oil.

Graph 5

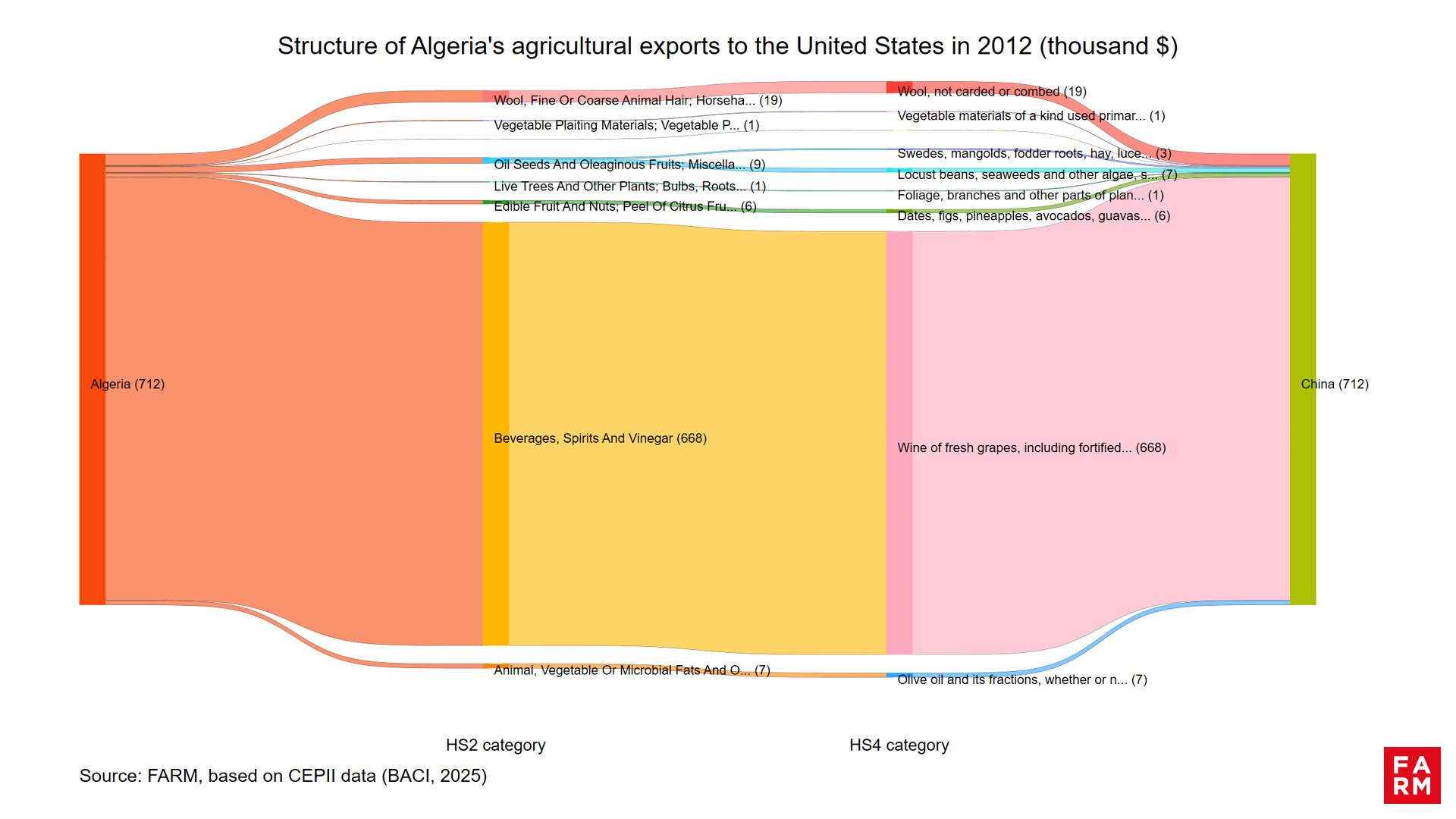

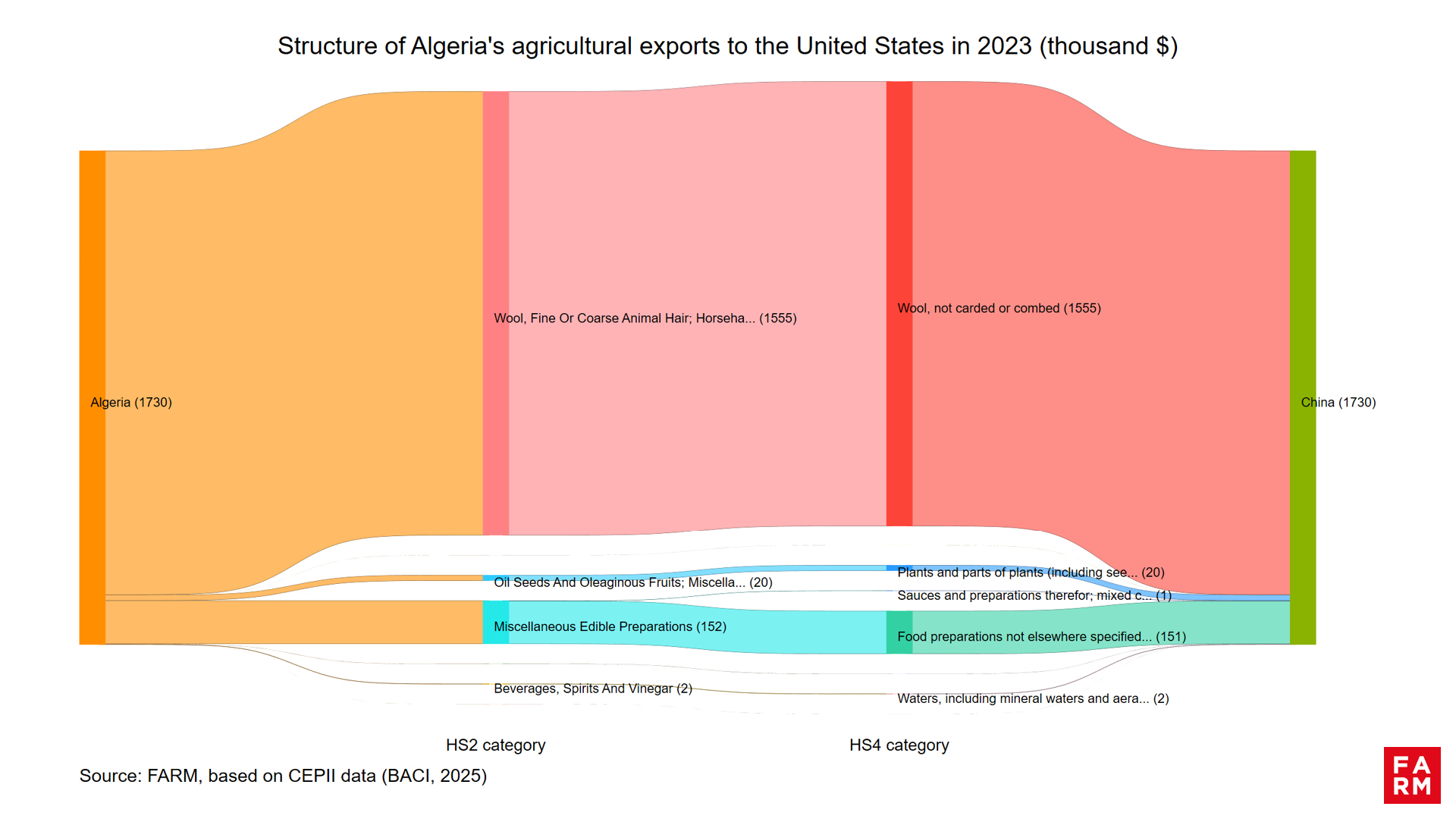

Algeria: integration still marginal

In 2012, Algerian agricultural exports to China amounted to 712,000 USD, composed almost exclusively of wines (nearly 94,% of exports). Some secondary flows existed, but at very low levels: wool, fruits and dates, oils and fats. Algeria's presence in this market was therefore limited and not very diversified.

In 2023, exports reach 1.73 million USD, an increase of + 143 %, but they remain marginal in the regional whole. The structure of the flows is however changing significantly:

- There raw wool, not carded or combed largely dominates, with 1.55 million USD, representing nearly 90 % of exports.

- Modest volumes appear in the various food preparations (152,000 USD).

- A few industrial and agricultural products (oilseeds, plants, drinks, mineral water) complete the basket, but in anecdotal proportions.

Algeria appears to be a minor player in regional agricultural exports with a decline of 22 % between 2012 and 2023, from 266 to 208 million USD.. Exports to China remain low. The removal of tariffs could provide an opportunity to promote niche products, such as dates.

Graph 6

Lessons for the region

The analysis of North African agricultural exports to China reveals several lessons:

- A dynamic of rapid growth, mais reposant fortement sur l’Égypte, qui concentre l’essentiel des exportations.

- An increase in added value, with the notable progression of processed products, even if raw materials still dominate.

- Differentiated trajectories by country : Egypt combines volumes, diversification and upgrading; Morocco is progressing but remains a secondary player; Tunisia is experiencing a decline in its emblematic sector and Algeria remains almost absent from the market.

While the UNITED STATES tighten their tariffs, the opening of China broadens the prospects for the region. But transforming this access into market share requires a diversification export sectors, and investments in distribution and promotion North African products to Chinese consumers. In this changing commercial landscape, current developments create both risks and opportunities for North Africa, but above all they remind us of the need to diversify the outlets and reduce dependence on a few strategic markets. The challenge is not to favor one partner over another, but to build resilient business strategies adapted to a rapidly changing international environment.

Table of distribution of agricultural exports in the North Africa region between 2012 and 2023

Un commentaire sur “Suppression des droits de douane chinois : quelles opportunités pour les exportations agricoles nord-africaines ?”