North Africa facing changes in global trade: what agricultural export strategies?

The recent rise in trade tensions on global markets, illustrated by the strengthening of tariff barriers in the United States, is a reminder of the complex challenges of a rapidly changing globalization landscape. In this unprecedented context, the FARM Foundation is continuing its regional analyses of African agricultural foreign trade, focusing on North Africa and its trade with the rest of the world. A second section will complement these analyses on trade relations with the United States and China.

Istanbul, ocean scene with cargo ship (©Freepik)

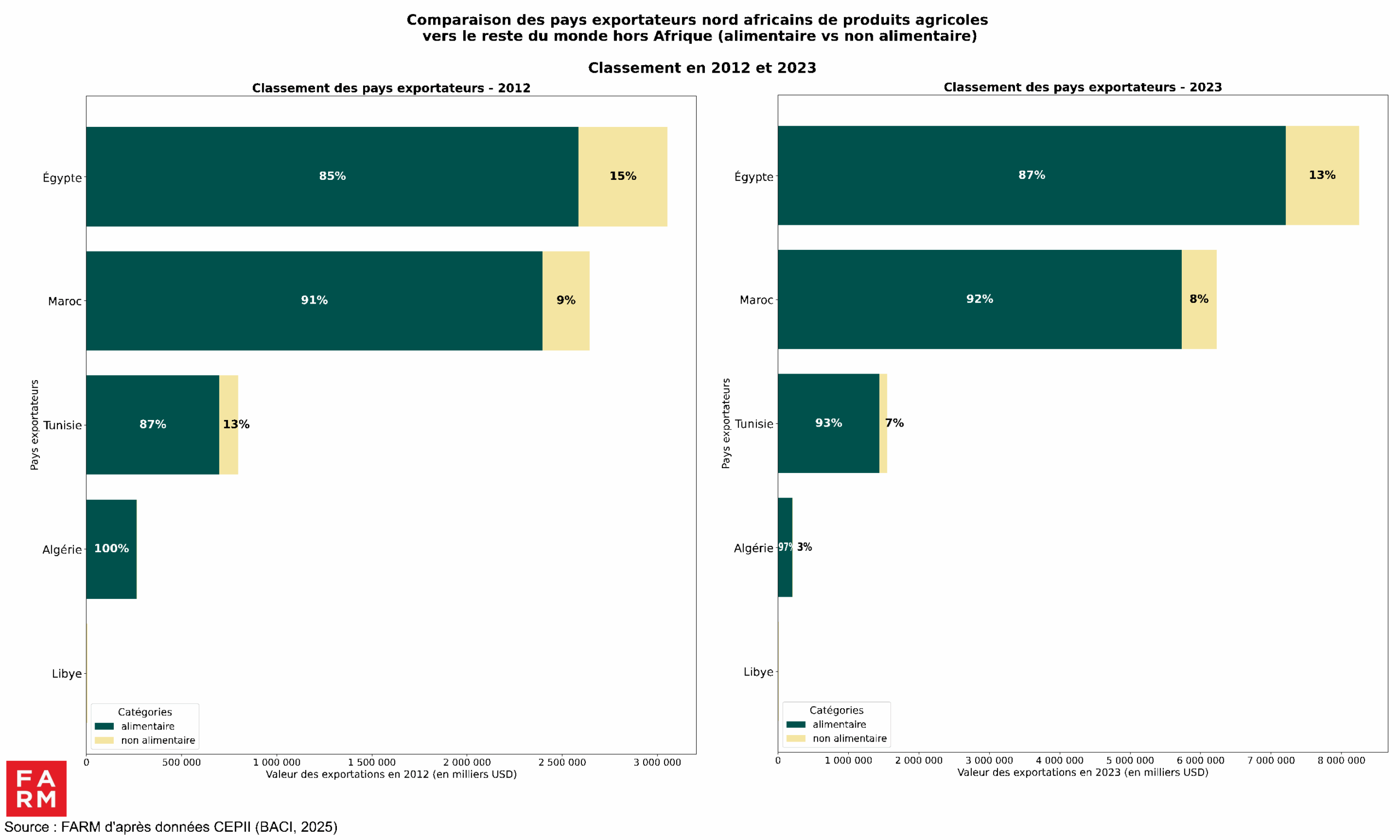

85 % of agricultural exports are food

Between 2012 and 2023, agricultural exports from North African countries to the rest of the world (outside Africa) more than doubled in value (+139 %), rising from nearly USD 6.8 billion to more than USD 16.24 billion.

When we look at the structure of exports agricultural from North Africa to the world (outside Africa), we see that they are largely dominated by food productsIn 2012 as in 2023, the situation remained comparable: more than 85 % of agricultural products exported by Morocco, Egypt, Tunisia or Algeria are edible foodstuffs (fruits, vegetables, olive oil, etc.).

Chart 1

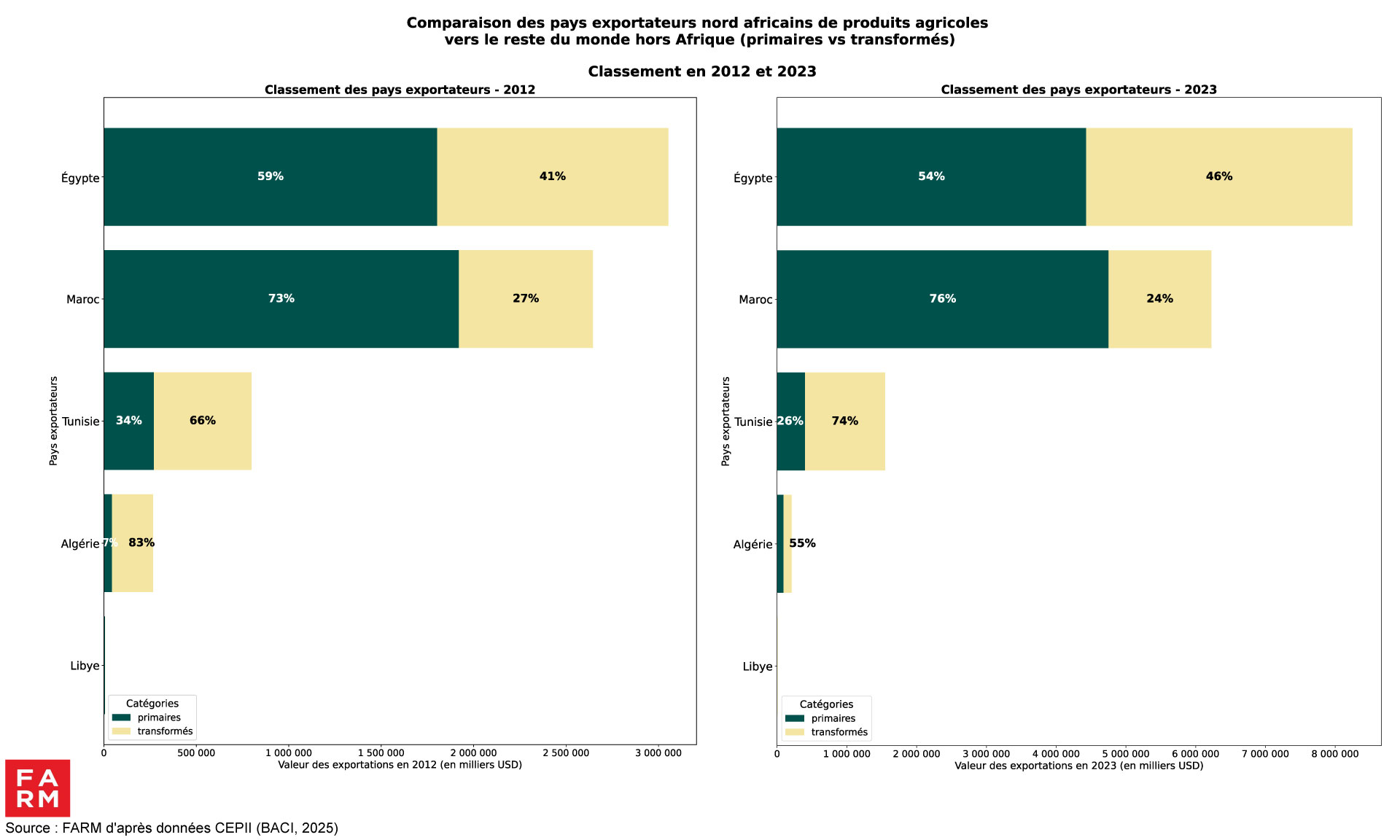

Processed products: a slow rise in range

If North Africa mainly exports food products, what about level of transformation of these products? Let us distinguish here the primary products (raw or minimally processed, such as fresh fruit, unprocessed cereals, raw agricultural products) and processed products (with higher added value, such as preserves, oils, food preparations, etc.). In this respect, the decade 2012–2023 shows some encouraging progress, although the predominance of primary education remains.

Egypt in the lead, but a transformation challenge still exists

Egypt stands out clearly as the leading North African agricultural exporter (nearly 51,% in 2023), with a spectacular growth in its agricultural exports to the world outside Africa (+170 %) in a decade. In 2012, these exports reached USD 3.05 billion, mainly composed of primary products (59 %). In 2023, this distribution remained relatively stable, with processed products then representing 46 %. The total value of exports has almost tripled to reach USD 8.25 billion. Egypt still has significant room to develop its agri-food industry and further increase its export added value.

Morocco, a heavyweight in raw materials

Morocco's agricultural exports are worth around 39 billion euros at the regional level. and have increased by 2.3 between 2012 (USD 2.65 billion) and 2023 (USD 6.2 billion). Despite this remarkable increase, the proportion of processed products in Moroccan agricultural exports remains lower, 27 % in 2012 and 24 % in 2023. This observation could reflect a strategic choice by the country to capitalize on its primary products (notably citrus fruits and fresh vegetables) while maintaining a stable, but moderate share of products with higher added value (oils, juices, etc.).

Tunisia focuses on processing and high value-added products

Tunisia with nearly 10 % of regional exports, displays a radically different dynamic from its neighbors, being the North African country most oriented towards processed agricultural products. In 2023, nearly three-quarters (74 %) of its agricultural exports were processed products, compared to 66 % in 2012. Tunisian agricultural products generate greater added value, thanks to emblematic sectors such as packaged olive oil. Other sectors of unprocessed products generate greater added value, such as dates. The total value of its agricultural exports has almost doubled, rising from $798 million in 2012 to around $1.55 billion in 2023 (+94 %). For Tunisia, the future challenge lies in consolidating these high-end markets and expanding its international outlets.

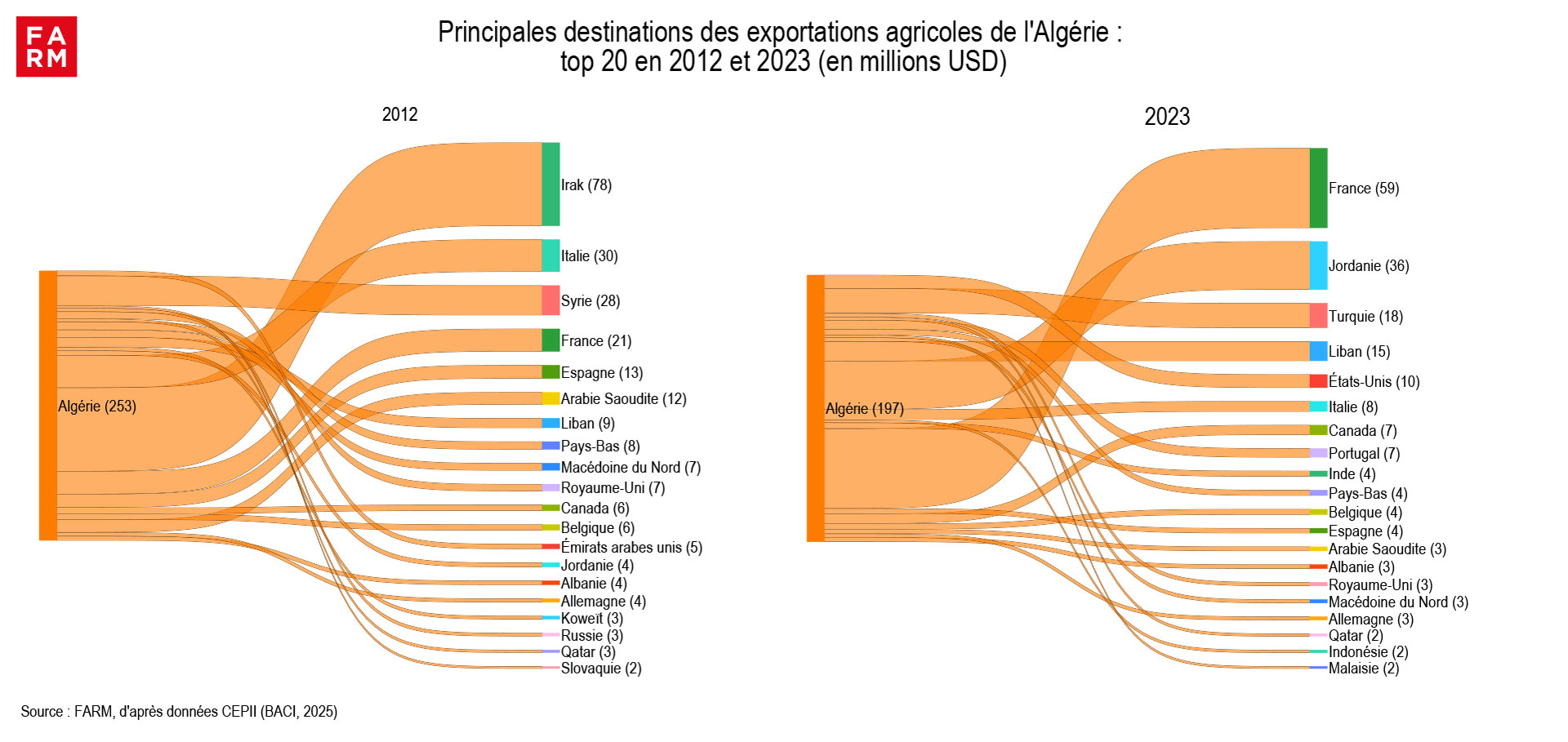

Algeria: Agricultural exports in decline, dominated by primary products

Algeria's trade dynamics contrast with those of its North African neighbors. Between 2012 and 2023, the total value of its agricultural exports decreased by 22 billion pounds, from $266 million to $208 million. Moreover, the share of processed products declined sharply, from $83 million to $55 million between 2012 and 2023.

Libya almost absent from regional agricultural exports

Finally, it is striking to note Libya's very low presence in these statistics. Its agricultural exports to the rest of the world outside Africa remain very low, reaching only $7 million in 2023, a slight increase of $1 million compared to 2012. This marginal figure could reflect the persistent impact of internal political crises, which significantly limit the country's agricultural development and export capacity.

Chart 2

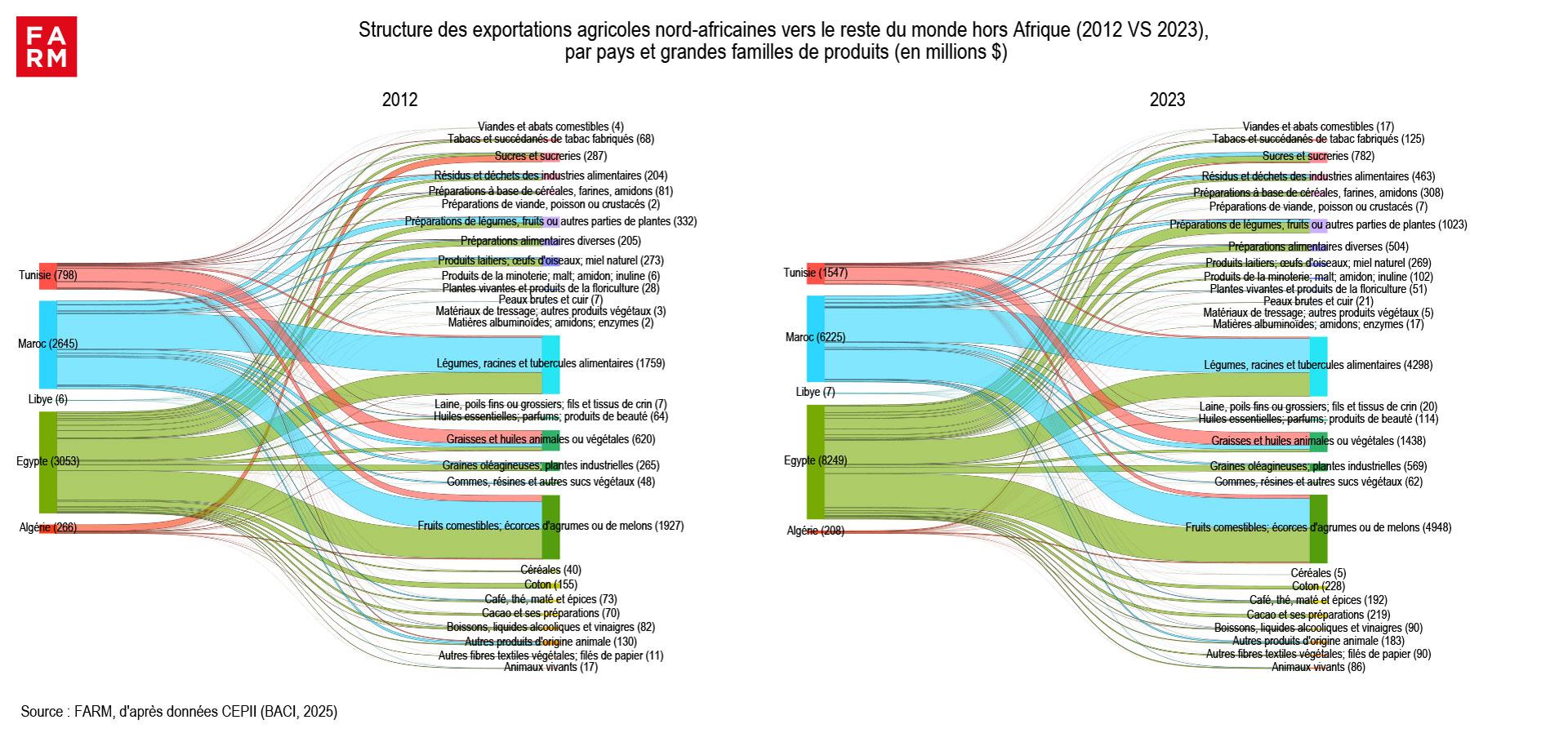

A marked specialization in fruits, vegetables and vegetable oils

North African agricultural exports to the rest of the world are dominated by three main sectors, each of which experienced remarkable developments between 2012 and 2023.

Edible fruits, citrus peel or melons (nearly 31,100 t of exports in 2023): + 156,100 t in 11 years

This category remains the most important, with a notable growth in exports, going from nearly 1.93 to 4.95 billion USD between 2012 and 2023. This dynamic illustrates the marked specialization of the region in Mediterranean and subtropical fruits, such as citrus fruits (oranges and mandarins), dates and more recently red fruits (raspberries, blueberries) as well as melons and avocados.

Vegetables, roots and tubers (nearly 27,100 tonnes of exports in 2023): + 144 %

This second major category also saw a sharp increase, from nearly USD 1.76 billion to USD 4.3 billion between 2012 and 2023. The region thus confirms its competitiveness in the export of fresh vegetables, in particular tomatoes, potatoes, onions, leguminous vegetables (green beans, peas), mainly intended for European markets. However, these exports come at the cost of very high water consumption and inputs, calling into question the sustainability of these agricultural and commercial choices.

Vegetable fats and oils (nearly 9,100 t of exports in 2023): + 132,100 t

Vegetable fats and oils are another strategic sector that is growing rapidly, growing from USD 620 million in 2012 to around USD 1.44 billion in 2023. This growth is mainly driven by olive oil Tunisian, flagship product with high added value.

In addition to these three major sectors, vegetable and fruit preparations (nearly 7 % of exports in 2023) are distinguished by spectacular growth: the value of their exports more than tripled between 2012 and 2023, rising from 332 million to more than 1.023 billion USD, a sign of a progressive transformation of the North African agrifood supply.

Chart 3

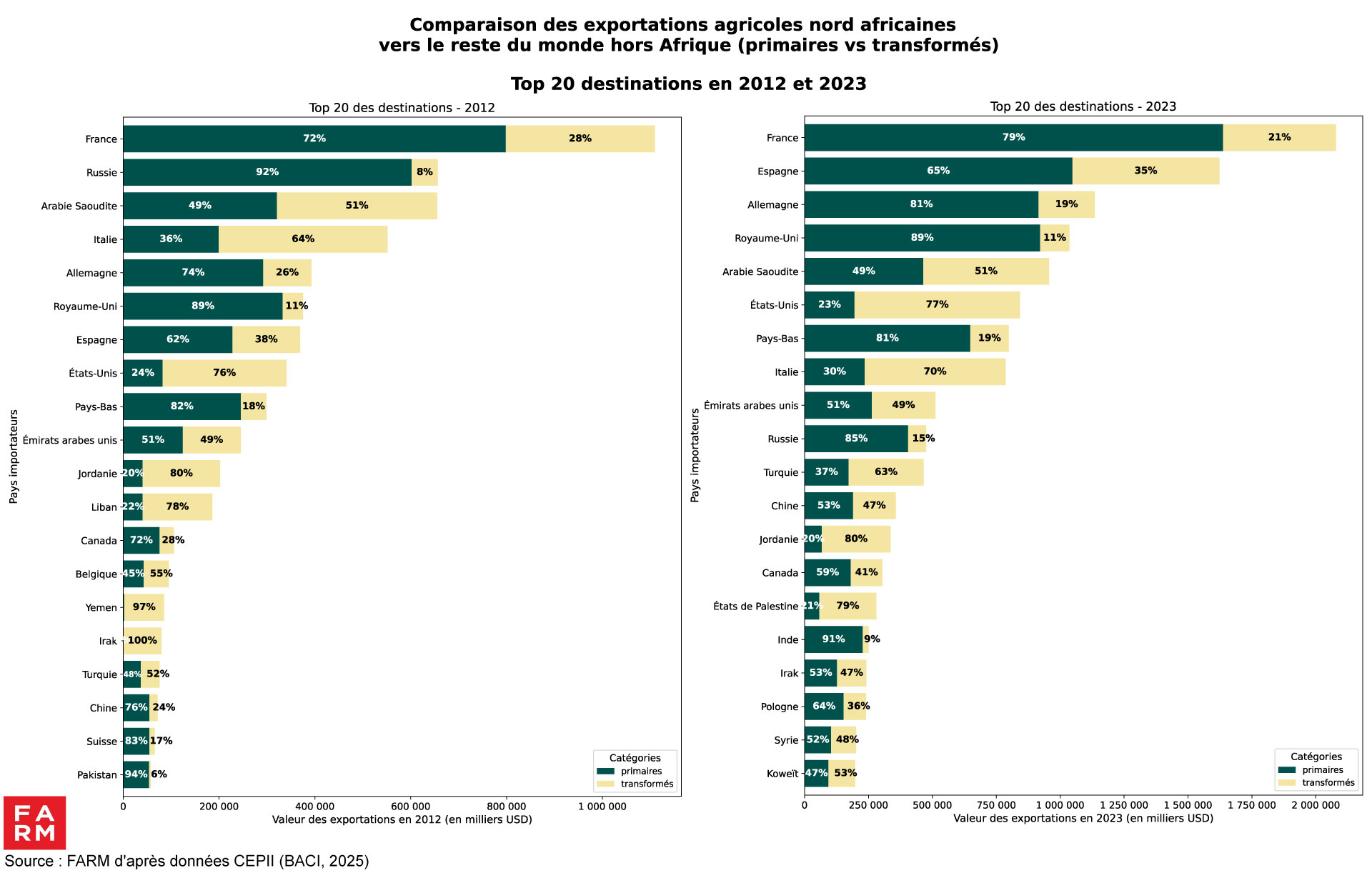

Main outlets: Europe remains predominant, Asian breakthrough and consolidation in the Middle East

Chart 4

Europe, a historic partner and primary regional outlet

In 2023, European countries accounted for 46.1% of North African agricultural exports to the rest of the world. This predominance is based on historical trade relations, facilitated by geographical proximity. The majority of exports to Europe concern products food (93 to 97 % depending on the country) and primary (65 to 89 %), such as fruits, vegetables, oils and dates.

-

- France : first market in 2023 with 2.08 billion USD, almost double compared to 2012 (1.11 billion). Exported products are 95 % food and to 79 % primaries.

- Spain : spectacular progression, multiplication by more than four of the exports (1.62 billion in 2023 compared to 369 million in 2012).

- Germany, United Kingdom, Netherlands : exports almost tripled for each of these countries, reaching USD 1.14 billion, USD 1.04 billion and USD 799 million respectively in 2023.

- Italy : more moderate growth (786 million in 2023 compared to 553 million in 2012), but with a specific feature: a more marked demand in processed products (70 %).

Gulf countries: growing demand for processed products

The Gulf countries are strengthening their role as major customers, together representing nearly 9 % of North African exports in 2023. Their demand is distinguished by a greater share of products transformed, particularly in higher value-added agri-food segments.

-

- Saudi Arabia : a stable partner (USD 956 million in 2023), with a balanced distribution between primary products (49 %) And transformed (51 %).

- United Arab Emirates : exports have more than doubled (from 245 million to 512 million USD), with an equally balanced composition between the two segments.

Other Middle Eastern countries show significant growth driven by processed products, such as Turkey (multiplication by 6, from 76 to 466 million USD) or the Jordan (from 202 to 336 million USD).

Breaking into new markets: United States, China and India

The last decade has seen the emergence of new extra-regional partners, with contrasting profiles:

-

- UNITED STATES : strong demand for processed products (77 %) and food (93 %), with exports increasing by 150 %, 340 to 843 million USD.

- China : a rapidly expanding market, exports have increased almost fourfold between 2012 and 2023 (from 72 to 357 million USD), with relatively balanced demand between primary products (53 %) And transformed (47 %).

- India : although still modest, the country is recording a exponential growth North African imports, multiplied by 73, passing from 3.4 million in 2012 to more than 250 million USD in 2023, mainly in primary products (91 %).

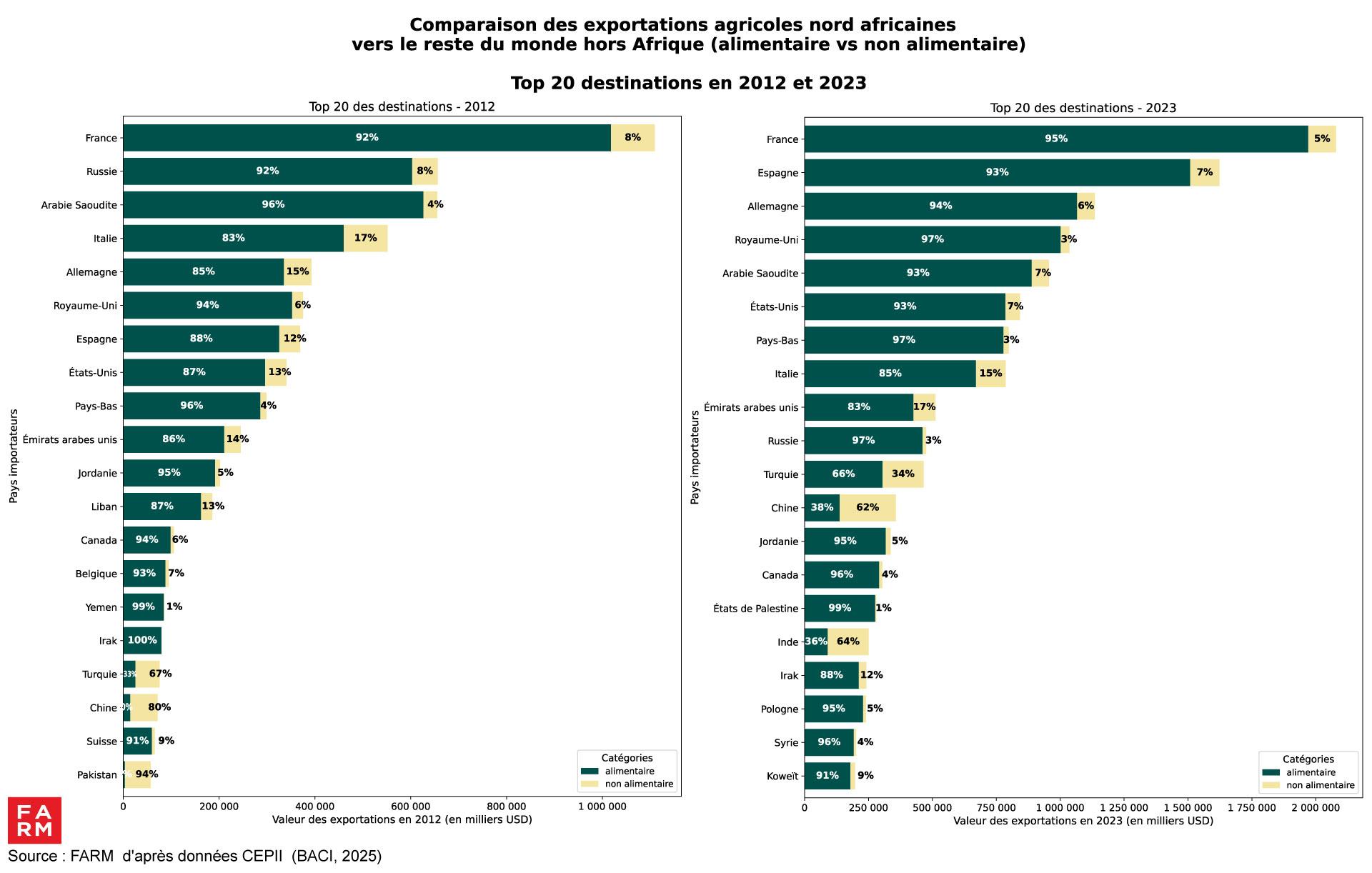

Exports dominated by food products, except to China and India

On average, more than 90% of North African agricultural exports to the rest of the world are foodHowever, some markets have more diversified demand:

-

- China (62 %), India (64 %) And Türkiye (34 %) display a significant share of products non-food, such as leathers, wools or plants for industrial use.

- Conversely, the main European, North American and Gulf markets largely favor products with food vocation.

Chart 5

Egypt: heading East and moving upmarket

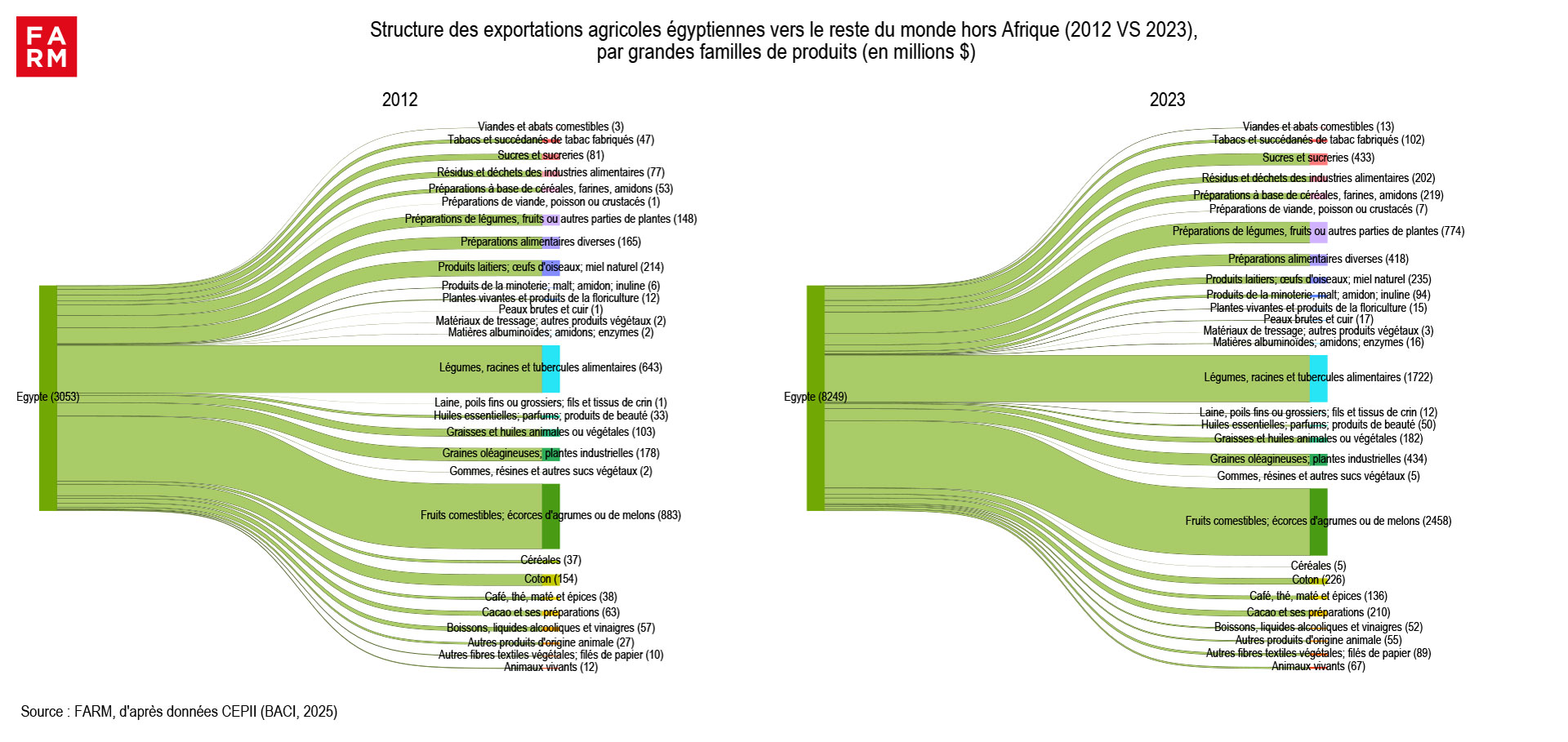

Egyptian agricultural exports are concentrated in two main categories (fresh fruits and vegetables), complemented by a third, which is booming (plant preparations). They position Egypt as a major player in agricultural exports in the region (nearly 51,% in 2023), capable of both supplying competitively priced fresh produce and gradually developing products with higher added value. The country is characterized by a geographical diversification of its outlets. The Gulf countries are a very important destination as markets towards Asia (China and India) and Europe are developing, strengthening the country's anchoring in global agricultural value chains.

Fresh fruits, vegetables and food preparations at the heart of export dynamics

-

- Edible fruits, citrus peel or melons (30 % of exports in 2023): multiplication by 2.7

This category is experiencing significant growth, rising from USD 883 million in 2012 to approximately USD 2.46 billion in 2023. This dynamic is notably driven by fresh citrus fruits (mainly oranges), reaching around USD 1.14 billion alone in 2023, as well as fresh and dried grapes, whose exports amount to USD 341 million.

-

- Vegetables, roots and tubers (21 % of exports in 2023): 2.7 times increase

This category is showing remarkable growth, growing from USD 643 million in 2012 to nearly USD 1.73 billion in 2023.

Fresh vegetables clearly dominate this category, including:

-

-

-

-

- potatoes (451 million USD);

- onions and other alliums (299 million USD);

- various other vegetables (including fresh or dried leguminous vegetables, frozen uncooked or boiled or steamed vegetables, tomatoes, etc.) representing more than USD 800 million.

- cassava roots, sweet potatoes and similar tubers show exceptional growth in value, increasing from USD 10 to 171 million between 2012 and 2023 (17-fold increase in a decade).

-

-

-

-

- Preparations of vegetables, fruits or other parts of plants (approximately 10 % of exports in 2023): from 148 to 774 million USD

This category is growing very strongly and suggests a desire among Egyptian players to transform their agricultural products. Exports of these preparations show remarkable growth (multiplication by 5 in a decade).

Chart 6

Egypt looks east to Asia for its markets

Chart 7

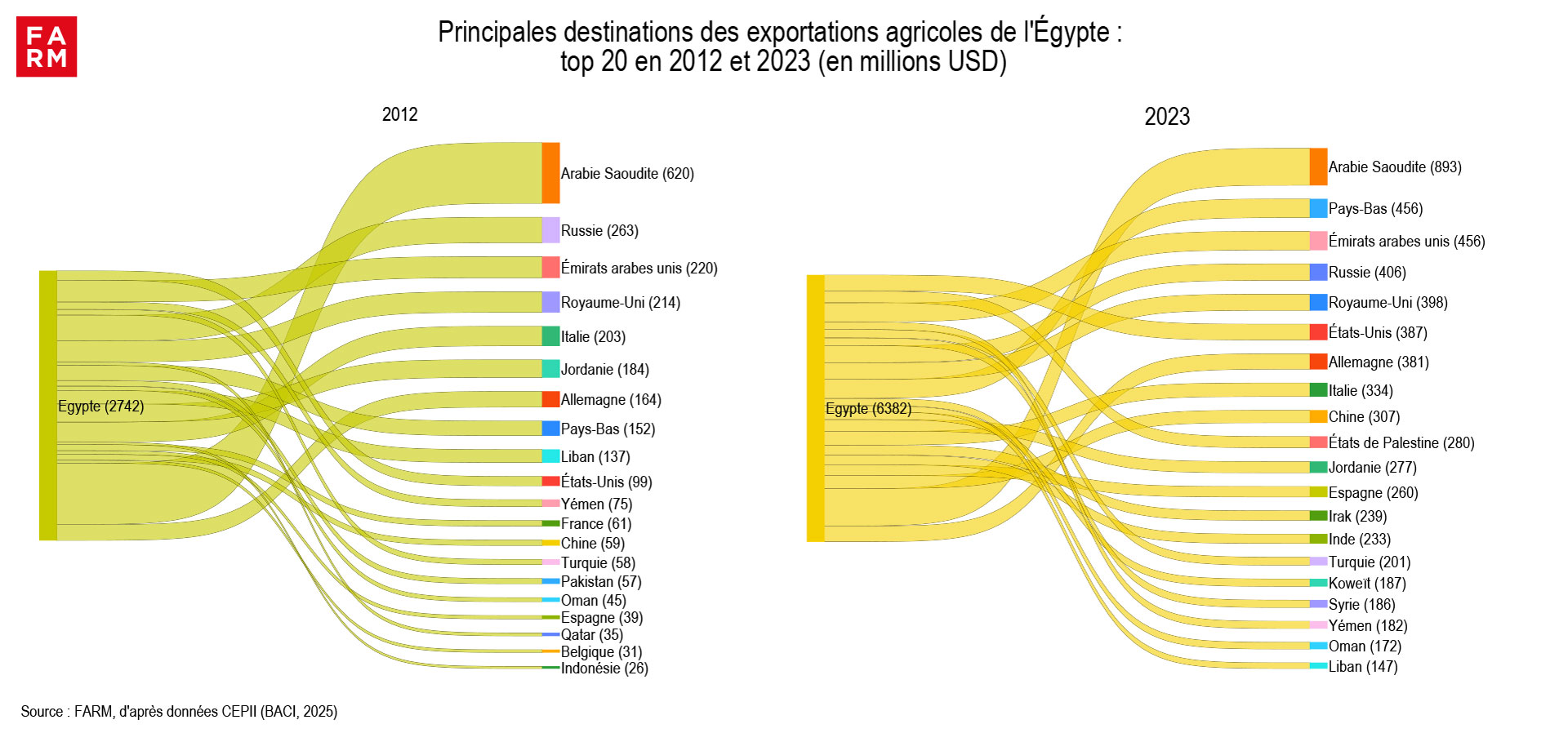

Between 2012 and 2023, Egypt significantly expanded and strengthened its agricultural export markets, with the total value exported to its top 20 partners more than doubling (from USD 2.74 billion to USD 6.38 billion). This momentum is accompanied by three notable trends:

-

- A strengthened anchoring in the Middle East: Saudi Arabia remains by far the leading destination, with nearly USD 900 million in 2023, up 44% compared to 2012. The United Arab Emirates, Jordan, Kuwait, Qatar, Yemen and Oman are also among the top customers, consolidating the central position of the Gulf as a preferred outlet. The entry of Palestine (USD 280 million) and Iraq (USD 239 million) into the top 20 reinforces this regional strategy.

-

- A notable breakthrough in Europe and Asia: The United Kingdom, Germany, Italy, and the Netherlands maintain significant values, with significant increases. The Netherlands triples its value between 2012 and 2023 (from USD 152 million to USD 456 million), while China becomes a major customer (from USD 59 million to USD 307 million). India (USD 233 million) also enters the ranking, reflecting a strategic expansion towards South Asia.

-

- An emergence towards new markets: Several previously marginal countries are recording strong growth, such as Turkey, Syria and Spain. The United States, although increasing (from 99 to 387 million USD), remains behind other partners.

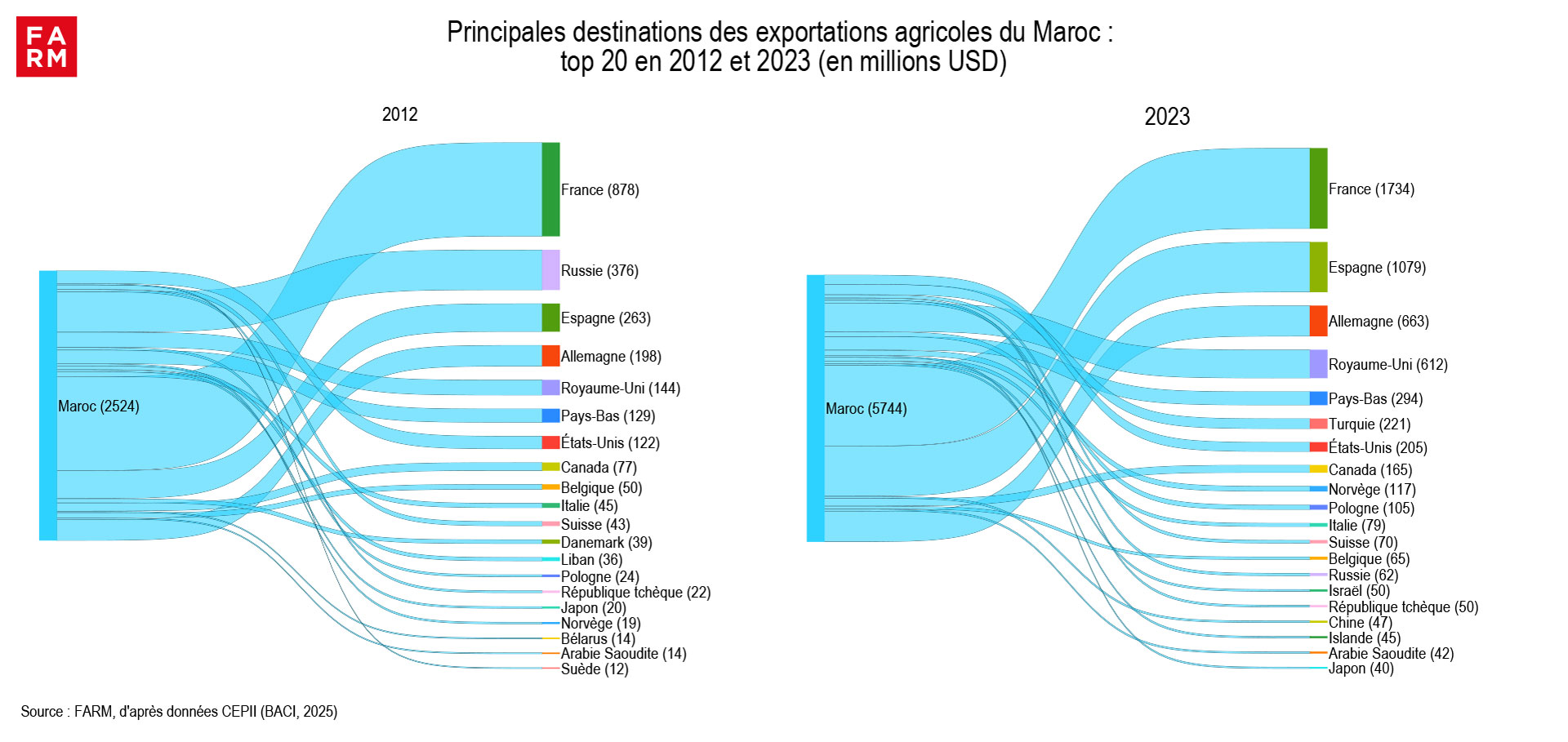

Morocco strengthens its position as a preferred supplier to the European market

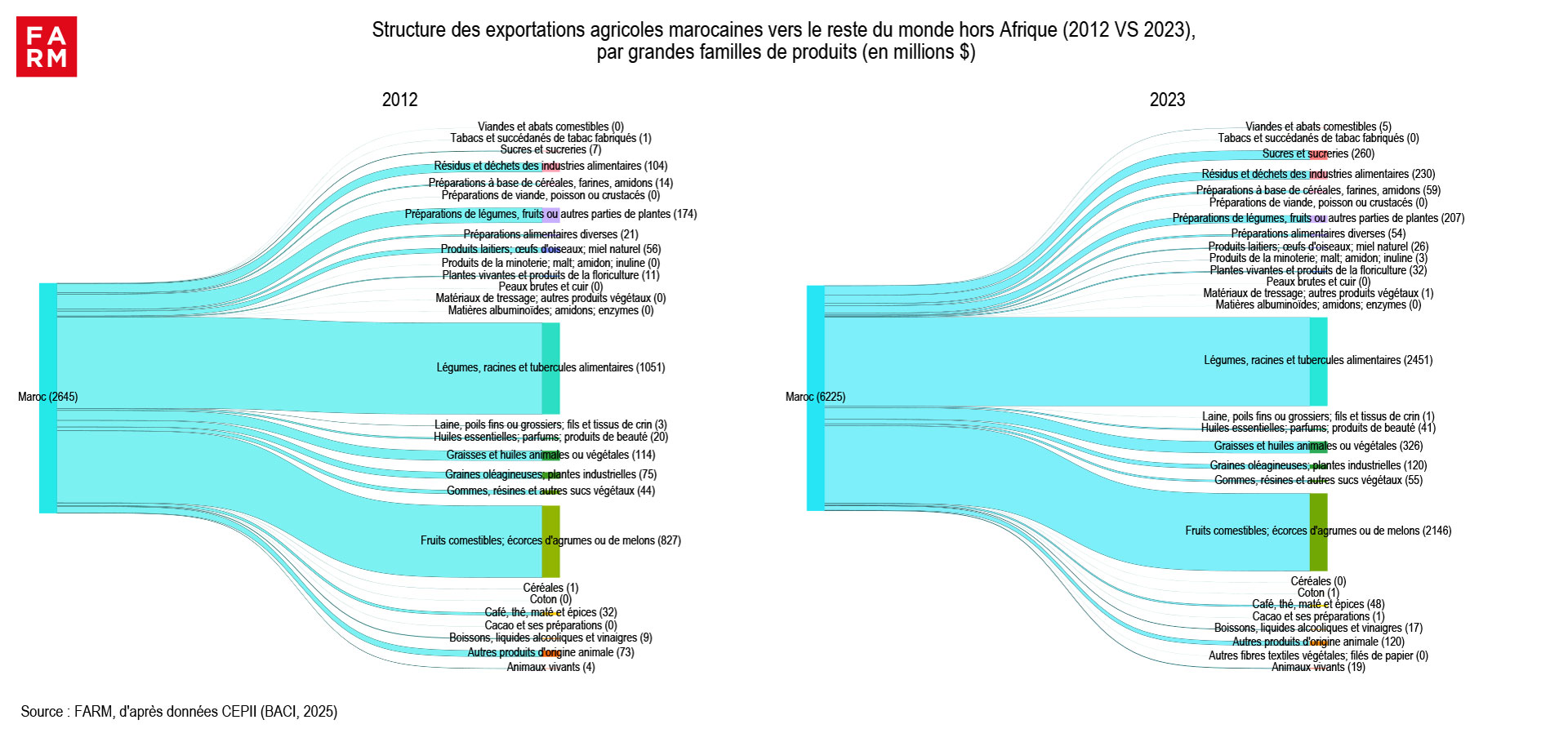

Morocco's agro-commercial profile is characterized by a strong concentration of its exports in two strategic segments: fresh vegetables and edible fruits. The country is diversifying its exports by developing new products with high potential (red fruits, avocados, melons, watermelons). Between 2012 and 2023, Morocco more than doubled the value of its agricultural exports to its 20 main partners. This growth was accompanied by a clear strengthening of its anchoring in the European market, which absorbs the overwhelming majority of its agricultural exports, and a diversification (Middle East, America, Asia) that is still limited. This positioning reflects both logistical advantages andpreferential agreements, but also raises the question of resilience in the face of possible commercial turbulence on the European market.

Confirmed specialization in fresh vegetables and increased diversification in fruits

-

- Vegetables, roots and tubers (39 % of exports in 2023): + 133 %

With a growth of 133 % between 2012 and 2023 (2.45 billion USD), these exports are mainly driven by tomatoes (+171 %) to reach USD 1.57 billion in 2023, now representing almost two-thirds of the category. Vegetables “shelled or unshelled, fresh or chilled” (beans, weights and others) also show a notable increase (+54 %), reaching USD 301 million in 2023.

-

- Edible fruits, citrus peel or melons (34 % of exports in 2023): multiplication by 2.5

Exports of these products have increased 2.5-fold, from USD 827 million in 2012 to more than USD 2.1 billion in 2023. Historically dominant, citrus fruits However, they show a modest increase (+8 % in ten years), reaching 509 million USD. Their relative weight in this category has decreased significantly, going from 57 % in 2012 to only 24 % in 2023.

This relative decline is explained by the remarkable rise in power of other fruits, notably red fruits, whose overall exports exploded from USD 113 million to USD 907 million. This category mainly includes:

-

-

-

- cranberries, blueberries and other small red fruits (441 million USD, 21 % of total edible fruits);

- raspberries (436 million USD, 20 1TP3Q of the total);

- strawberries (USD 85 million, 4 % of the total), which represented nearly 60 % of red fruit exports in 2012, but only 9 % in 2023.

-

-

At the same time, exports of melons and watermelons are also experiencing very strong growth, going from USD 68 million to USD 283 million (13 % of the category total). The lawyers also emerging as a booming sector, with exports increasing more than 50-fold, from USD 4 million to USD 208 million (10 % of the category total).

Chart 8

European anchoring and opening towards Asia and America

Chart 9

-

- A strong presence on the European market:

France, Spain, Germany, the United Kingdom, and the Netherlands account for nearly 75 billion pounds of Moroccan agricultural exports. France remains by far Morocco's largest trading partner, with a volume that doubled between 2012 and 2023 (from USD 878 million to USD 1,734 million). Spain is experiencing spectacular growth, rising from USD 263 million to over USD 1,079 million, ranking second. The other three countries also show notable increases, confirming the Euro-Mediterranean orientation of the country's trade strategy.

-

- Secondary outlets, but growing in North America, the Middle East and Asia

The United States appears in eighth place with USD 205 million in 2023, an increase compared to 2012 (USD 122 million), just ahead of Canada, which doubled the amount of its imports. However, they are still far behind their European partners. Turkey (USD 221 million), China (USD 47 million), Japan (USD 40 million), and Israel (USD 50 million) are now among the main customers, reflecting a geographical diversification that is still modest, but under construction.

-

- A significant withdrawal from Russia:

Russia, which was in second place in 2012 (USD 376 million), will fall to thirteenth place in 2023 with only USD 62 million. Logistics issues as well as fluctuations in the ruble may have contributed to the erosion of this trade.

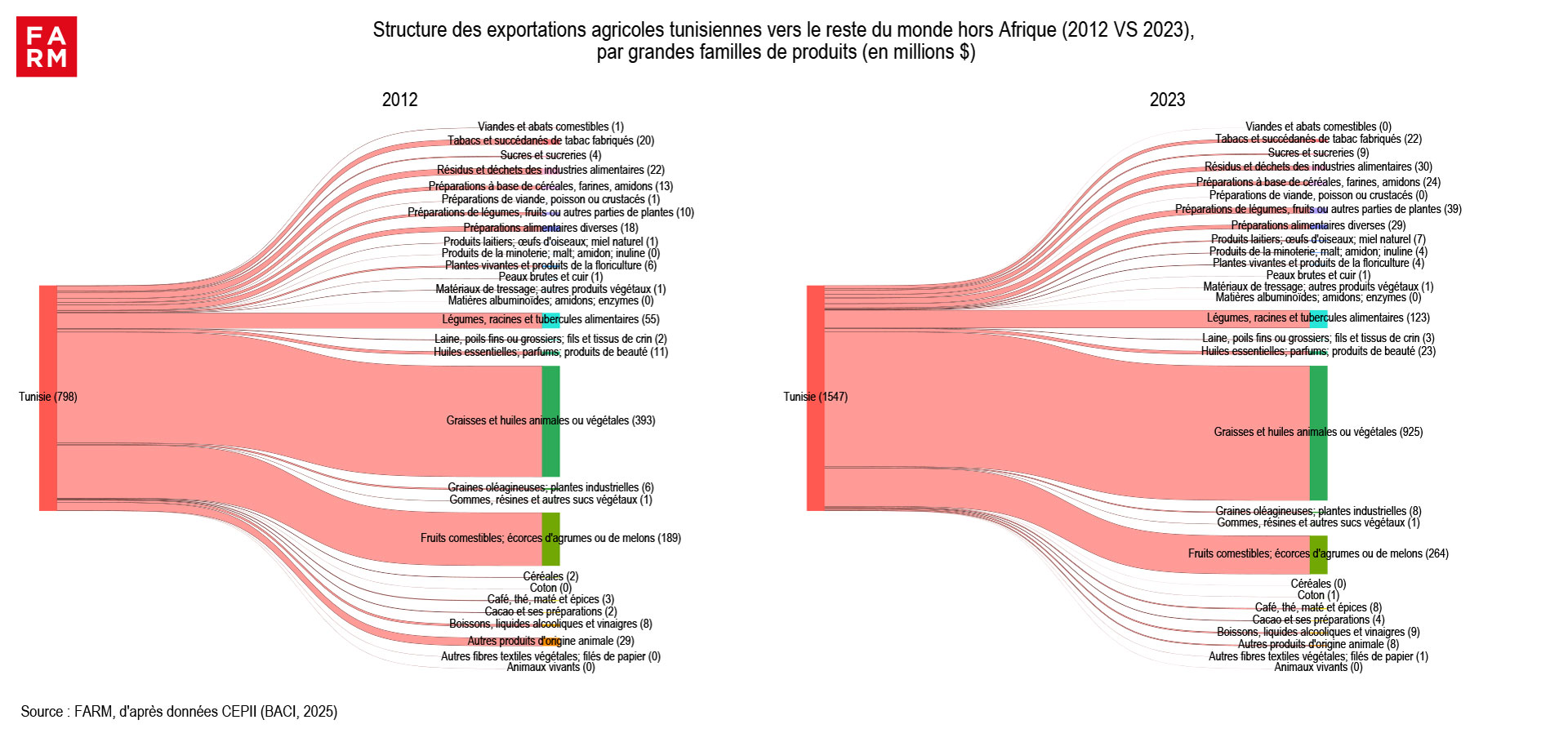

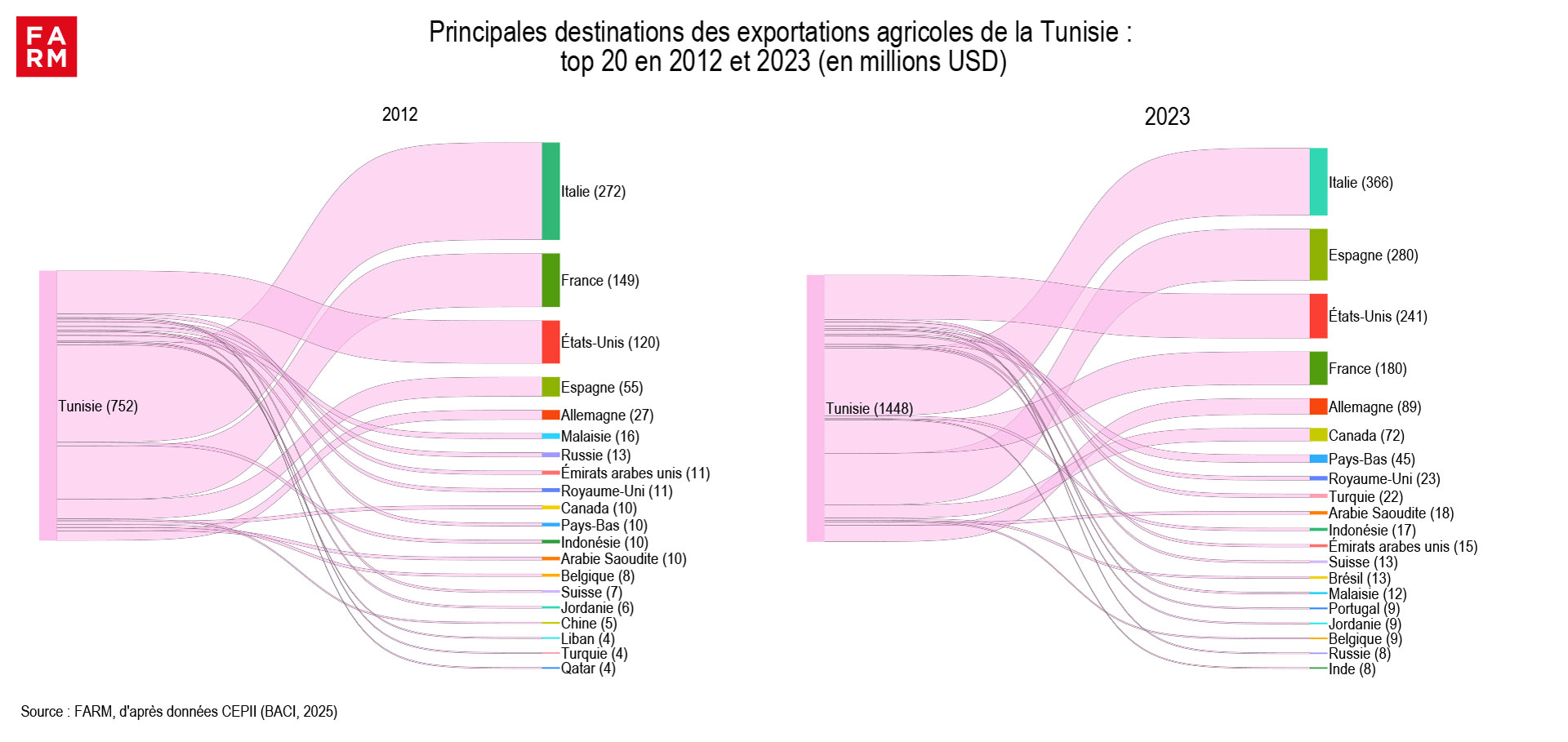

Tunisia: the (slow) march towards diversification

Between 2012 and 2023, Tunisian agricultural exports to its 20 main partners increased from USD 752 million to nearly USD 1.45 billion, an increase of 92.1%. Tunisian agricultural exports have historically been dominated by olive oil and dates. They are now complemented by a gradual diversification into fresh vegetables. This strategic combination allows Tunisia to consolidate a qualitative specialization with high added value, while gradually expanding its range of exportable products on the international market. Overall, Tunisia's positioning is both consolidated in Europe and expanding towards North America, which strengthens the visibility of its agricultural sectors. Opening up to new Asian markets remains marginal, highlighting significant room for growth to further diversify commercial outlets.

Olive oil and dates, pillars of exports

-

- Vegetable fats and oils (60 % of exports in 2023): multiplication by 2.35

This category is dominated primarily by olive oil. The value of these exports has more than doubled in a decade, rising from USD 393 million in 2012 to approximately USD 925 million in 2023. This dynamic confirms the international reputation of Tunisian olive oil, which is highly prized, particularly by buyers from southern Europe who re-export it, sometimes capturing a share of its added value.

-

- Edible fruits (17 % of exports in 2023) : + 40 %

Dates represent the vast majority of this category, showing growth of more than 40% in a decade, from USD 189 million in 2012 to USD 264 million in 2023.

-

- Vegetables, roots and tubers (8 % of exports in 2023): + 127 %

This emerging category has experienced significant growth (+127 % in more than 10 years), reaching USD 123 million in 2023. This dynamic is driven in particular by tomato exports, representing the majority of this category with USD 91 million.

Chart 10

Europe, main outlet for Tunisian exports and growth of the North American market

Chart 11

-

- A strong European anchorage

Europe remains the leading regional market, with Italy in the lead (USD 366 million in 2023 compared to USD 272 million in 2012), followed by Spain (USD 280 million compared to USD 55 million in 2012) and France (USD 180 million compared to USD 149 million). Germany (USD 89 million) is also in the top 5.

-

- A rise in power of the United States

In 2023, they will become Tunisia's third-largest trading partner for agricultural exports (USD 241 million), almost doubling their value compared to 2012 (USD 120 million). This increase reflects a growing demand for Tunisian products with high added value, particularly olive oil, in a North American market with strong demand for quality Mediterranean products.

-

- Diversified, but still modest, secondary markets

Canada (USD 72 million), the Netherlands (USD 45 million), the United Kingdom (USD 23 million), Saudi Arabia, Turkey, and the United Arab Emirates appear in the 2023 ranking, but do not reach the levels observed in other EU countries or the United States. Other countries such as Brazil, Malaysia, Portugal, and Russia are in the top 20, with amounts that are still limited.

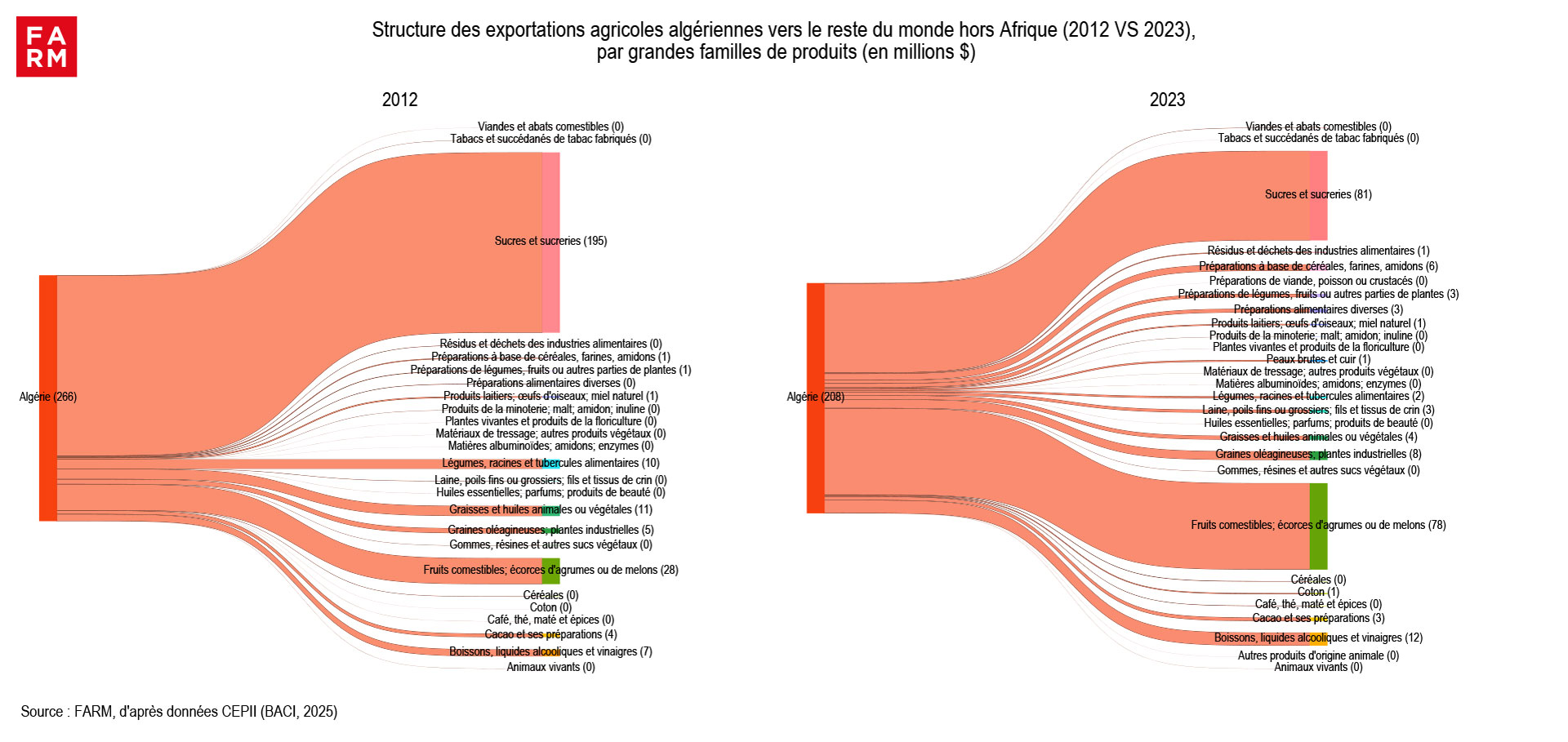

Algeria: duality and recomposition of agricultural exports

Between 2012 and 2023, the structure of Algeria's agricultural exports was marked by a strong duality between sugars and dates, which together accounted for nearly 77% of the total exported value in 2023. Sugar exports, historically dominant, experienced a sharp decline (- USD 114 million), while edible fruits, mainly dates, increased dramatically to reach USD 78 million. This development was accompanied by an overall decline in the value of agricultural exports, which fell from USD 266 to 208 million over the period, a decrease of 22%, and a geographical narrowing of outlets, with increased concentration on a few markets such as France, Jordan and Turkey. Former major partners saw their importance fade. Despite some attempts at diversification into secondary markets, volumes remain low, reflecting the structural weakness of exportable supply and the lack of consolidation of competitive sectors internationally, in contrast to its regional neighbors.

Setback sugars and the rise of dates

-

- Sugars and sweets (39 % of exports in 2023): – 59 % of growth

This category, previously very dominant, is experiencing a sharp decline, falling from USD 195 million in 2012 to only USD 81 million in 2023. Exports mainly concern cane or beet sugar and chemically pure sucrose in solid form (around 95 % of the category), the remainder being molasses resulting from refining or extraction.

-

- Edible fruits (nearly 38 % of exports in 2023): 28 M to 78 M USD

Driven almost exclusively by dates, this category shows remarkable growth of more than 178 % over the period, reaching 78 million USD in 2023, of which 75 million comes from dates. Other exported fruits, mainly melons (excluding watermelons), remain very marginal.

Chart 12

A refocusing of outlets on France, Jordan and a few niche partners

Chart 13

-

- Recomposition of the leading trio with France in first position

In 2023, France is the leading partner for Algerian agricultural exports (USD 59 million), whereas it only occupied fourth position in 2012 (USD 21 million). Jordan follows with USD 36 million, a sharp increase compared to 2012, as does Turkey (USD 18 million). These markets, although relatively increasing, remain modest in absolute value and reflect a restructuring of flows rather than an expansion.

-

- Decline of historic destinations and limited diversification

Major partners in 2012 such as Iraq (78 M USD), Syria (28 M USD), Italy (30 M USD) and Spain (13 M USD) saw their role significantly reduced in 2023. Some, such as Iraq or Syria, disappear completely from the top 5, reflecting a loss of access or competitiveness in these markets. The rest of the ranking is made up of a very fragmented set of secondary markets (Canada, Portugal, India, the Netherlands, Belgium, etc.), each weighing less than 10 M USD.

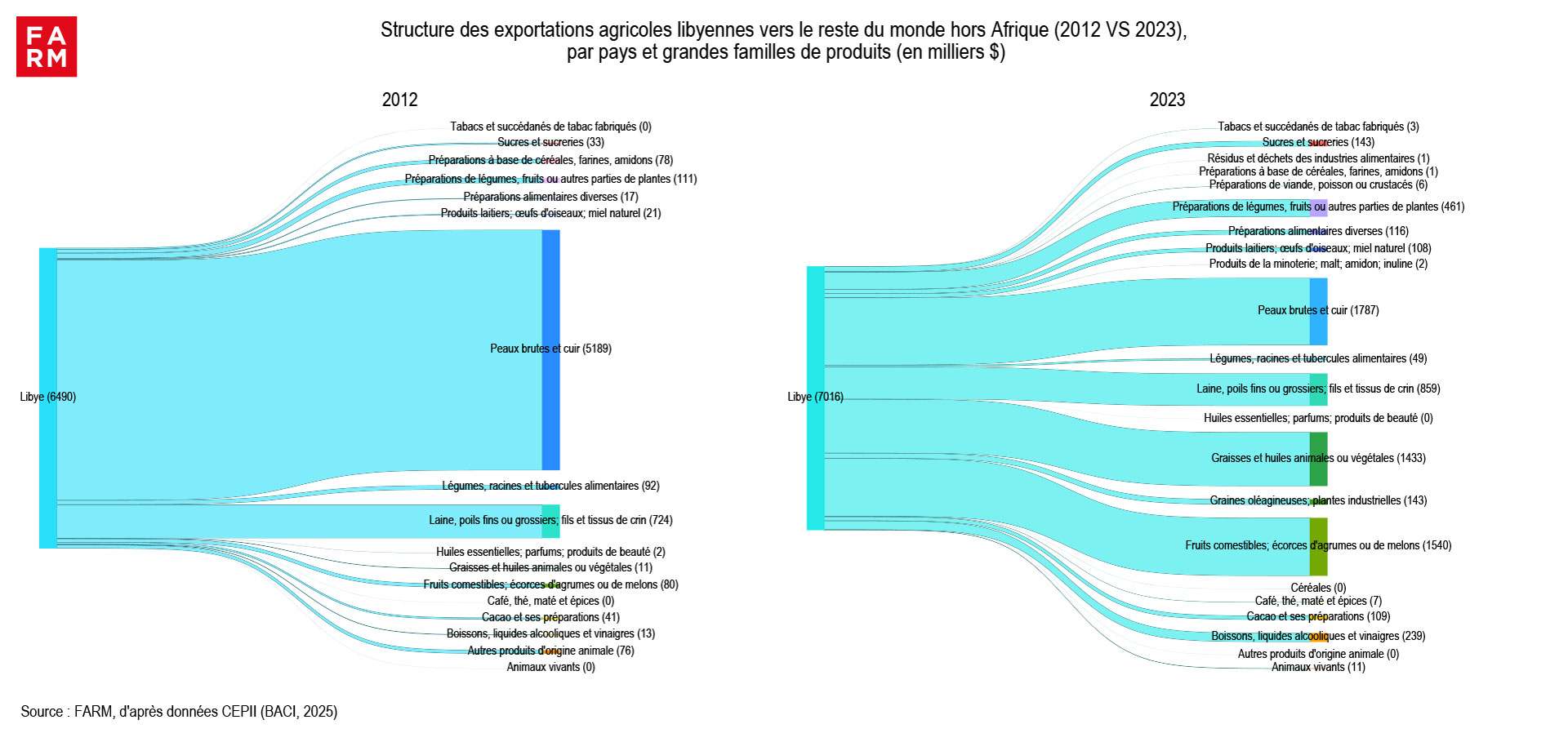

Transformation of the structure of agricultural exports in Libya

Between 2012 and 2023, Libyan agricultural exports are distinguished by their very low overall value (around USD 7 million in 2023) and by a gradual transformation of their composition, in a context of strong political instability hampering the development of the sector. Libya has moved from agricultural exports dominated by hides and skins to a more diversified structure, with the rise of dates and olive oil, while animal fibers remain stable.

Despite this sectoral diversification, Libya remains marginal on the regional scene, its agricultural exports remaining limited in volume and value. Geographically, Turkey remains by far the main outlet (41,% of the total in 2023, compared to nearly two-thirds in 2012), while Italy, a historic partner, is seeing its weight decline. We are seeing the emergence of new Asian partners (Indonesia, India, Malaysia), reflecting a timid but real diversification of markets, although the amounts remain modest.

A marked decline in leather exports, with an emergence of dates and olive oils

-

- Raw hides and leather (25% of exports in 2023): – 65 % growth

Historically dominant, this category represented nearly 80,000 tonnes of Libyan agricultural exports in 2012, with USD 5.2 million. It has experienced a marked collapse, falling to USD 1.8 million in 2023. Although in sharp decline, it remains the leading export category.

-

- Edible fruits (22 % of exports): 19-fold increase

Mainly driven by dates, this category will become the second pillar of Libyan agricultural exports in 2023, reaching USD 1.54 million compared to only USD 80,000 in 2012, a multiplication by almost 19 in a decade.

-

- Vegetable fats and oils: 20% of exports

Virtually non-existent in 2012 (USD 11,000), this category is growing strongly to reach USD 1.43 million in 2023, driven by olive oil exports.

-

- Wool and hair: 12 % of exports in 2023

The animal fiber category is holding up, with raw wool exports slightly up (from USD 724,000 to USD 859,000), still representing a significant share of the total.

Chart 14

Limited geographic diversification around Turkey, Southeast Asia and Italy

Chart 15

-

- Turkey, Libya's main agricultural trading partner

In 2012, Turkey alone accounted for nearly two-thirds of Libyan agricultural exports (USD 4.4 million out of 6.5 million). This dependence will remain strong in 2023, with USD 2.9 million, or approximately 41 billion of the total, although its relative weight has decreased.

-

- Historical partner in decline and emergence of new partners in Asia

While Italy, Libya's long-standing partner, is seeing its imports fall from USD 1.5 million in 2012 to USD 658,000 in 2023, South and Southeast Asia (Indonesia, India, Malaysia) are showing a gradual rise in importance. These breakthroughs signal a tentative diversification into Asian markets, probably linked to new trade channels or a search for outlets outside Europe.

Conclusion

In summary, North Africa sells primarily to Europe, its traditional partner, while expanding its horizons to the East and America. This geographic diversification is an interesting development, as it reduces dependence on a single market and offers growth drivers. It is particularly important at a time when the American market is tending to close and the Chinese market is opening up.