West Africa faces the nitrogen challenge: dynamics, dependencies and opportunities

Nitrogen, represented by "N" in the NPK formulation of mineral fertilizers, is fundamental for agricultural production, especially during the vegetative development phase of plants. It stimulates their growth and plays a key role in photosynthesis, making it an essential element in ensuring food security and agricultural sovereignty, both in West Africa and globally. FARM provides an initial analysis of West Africa's place in the global nitrogen market.

In May 2024, African Union Heads of State met in Nairobi, Kenya, to assess progress made since the 2006 Abuja Declaration on Fertilizers for the African Green Revolution. This meeting, which culminated in the signing of the Nairobi Declaration, highlighted several important points. Fertilizer use in Africa did increase, but it only rose from 8 to 18 kg/ha, well below the target of 50 kg/ha. The summit also highlighted the continent's dependence on international fertilizer markets, as well as the significant impact of the recent global crisis and the Russo-Ukrainian conflict, which led to a 25 % decrease in fertilizer consumption.

In this context, the FARM Foundation proposes an analysis of the evolution of nitrogen (N) trade flows and the place of West African countries in global trade. By presenting a map of these flows and exchanges, we will seek to identify the trade strategies adopted by certain countries in the region, as well as the forces at play, taking into account the opportunities specific to each country. This work shows the disparities between countries in the region regarding their autonomy in nitrogen fertilizers in order to assess the nitrogen dependencies of the countries in the sub-region and explore future possibilities for autonomy. This analysis aims to provide an understanding of the regional and national dynamics that influence nitrogen trade flows, while considering the implications for the future of agriculture in the region.

Mapping methodology

This analysis examines the evolution of average annual nitrogen exchanges between West Africa and the rest of the world (7 major geographical areas) over a 30-year period, from 1990 to 2022. The data are presented in the form of maps representing three distinct decades: 1990-2000, 2001-2011 and 2012-2022. Each map illustrates average annual flows, smoothed over a decade.

The flows concern pure mineral elements and not their commercialized fertilizer form. This approach offers a perspective on mineral element cycles in the region. The data are taken from the FAOSTAT database (2024). The analyses are carried out for the three elements, N, P and K (see other FARM publications on phosphorus And potassium).

The maps present three pieces of information. Imports from each country in the sub-region via histograms to the left of the maps. Exports from each country are modeled by arrows of varying thickness depending on the volume of flows. Consumption from each country in the West African sub-region is modeled by a flat color of varying intensity depending on the volume consumed.

West Africa, a marginal player in the global nitrogen market

Nitrogen consumption in West Africa has steadily increased since 1990, from an annual average of 254,279 tonnes over the period 1990–2000 to 677,306 tonnes per year over the period 2012–2022. This growth reflects an intensification of agricultural practices.

Imports followed a similar trend, increasing from 345,016 tonnes per year in the 1990s to 815,015 tonnes in the period 2012-2022. This increase indicates a growing dependence on external sources of nitrogen and nitrogen fertilizers to meet agricultural needs in the region. In 2022, West Africa imported 1 million tonnes of nitrogen, while in the same year France imported nearly double that amount, and India and Brazil 6 times more. The United States also ranks among the top 4, with 3.6 million tonnes of nitrogen imported in 2022.

Exports from individual countries have also seen notable growth, especially in the last decade, from 129,843 tonnes per year in the 1990s to 585,805 tonnes in the period 2012-2022. This increase suggests an improvement in regional nitrogen production and distribution capacities as well as increasing integration into the global nitrogen market.

Despite significant increases in both imports and exports, West Africa remains a marginal player internationally, accounting for 1.2 billion tonnes of global nitrogen imports and 3 billion tonnes of global nitrogen exports. These data highlight both the progress made by some countries in terms of production and exports, but also the strategic opportunity that this sector represents for countries in the region. Indeed, regional demand for nitrogen fertilizers is high, and the current low market share offers significant growth potential.

Evolving business partnerships

Analysis of nitrogen trade flows in West Africa reveals a significant change in trading partnerships over time. In the initial period (1990-2000), European countries occupied a dominant position, accounting for 43 billion tonnes of the subregion's total imports. The five main importing countries in West Africa had Europe as their main partner. One might think that this trade relationship would be linked to the post-colonial legacy, but of the 1.6 million tonnes imported during this period, France and Great Britain only contributed 106,665 tonnes, or only 6.6 billion tonnes. In contrast, Albania supplied nearly 20 billion tonnes of West Africa's nitrogen imports from Europe (mainly to Nigeria). Albania then had a production capacity that, after the fall of the USSR and the opening of its economy, was directed towards other geographies than the communist bloc of Eastern Europe. However, after 1991, Albania experienced a difficult period of economic transition that led to the destruction of many industries, including those related to fertilizer production, not making this country a long-term partner. In the case of Senegal and Côte d'Ivoire, the majority of nitrogen imports came from Germany or the Netherlands. This distribution suggests that market opportunities dictated the pattern of trade rather than historical and political ties.

The following period (2001-2011) saw a notable intensification of import flows marked by a gradual change in partners. European countries saw their importance decrease by a few points (43 to 38 %) in favor of Russia and the Black Sea. The share of imports from West African countries from this region doubled (from 14 to 28 %). In addition, during this period, Central and Eastern European countries (Bulgaria, Hungary, Romania) experienced a sharp increase in their consumption, requiring purchases particularly from European producer countries which, like Germany, were experiencing a decline in their consumption. Regarding exports, the three main exporters – Nigeria, Senegal and Côte d'Ivoire – maintained their position, while other countries began to participate in exports, albeit to a lesser extent.

The most recent period (2012-2022) seems to indicate an acceleration in the reconfiguration of import sources. Russian nitrogen has taken a predominant place, reducing the share of European nitrogen. It should also be noted that from 2014, the European Union became net importer of ammonium nitrate and that, over the period, it remains dependent for approximately 30 % on its consumption of nitrogen fertilizers, from Russia, Egypt and Algeria.

How should we interpret these developments? Are they the result of proactive strategies or the consequence of a complex competitive environment in which West African countries lack sufficient weight and therefore market power? On the one hand, West African countries are seeking to reduce their dependence on certain nitrogen exporters. On the other hand, these changes may be the result of external factors, such as changes in the trade policies of major partners, fluctuations in global markets, or geopolitical changes, such as the aforementioned collapse of the USSR. Furthermore, countries in the region, faced with small economies, limited production capacities, and a less developed industrial sector, may find themselves in less advantageous positions to satisfy their calls for tenders.

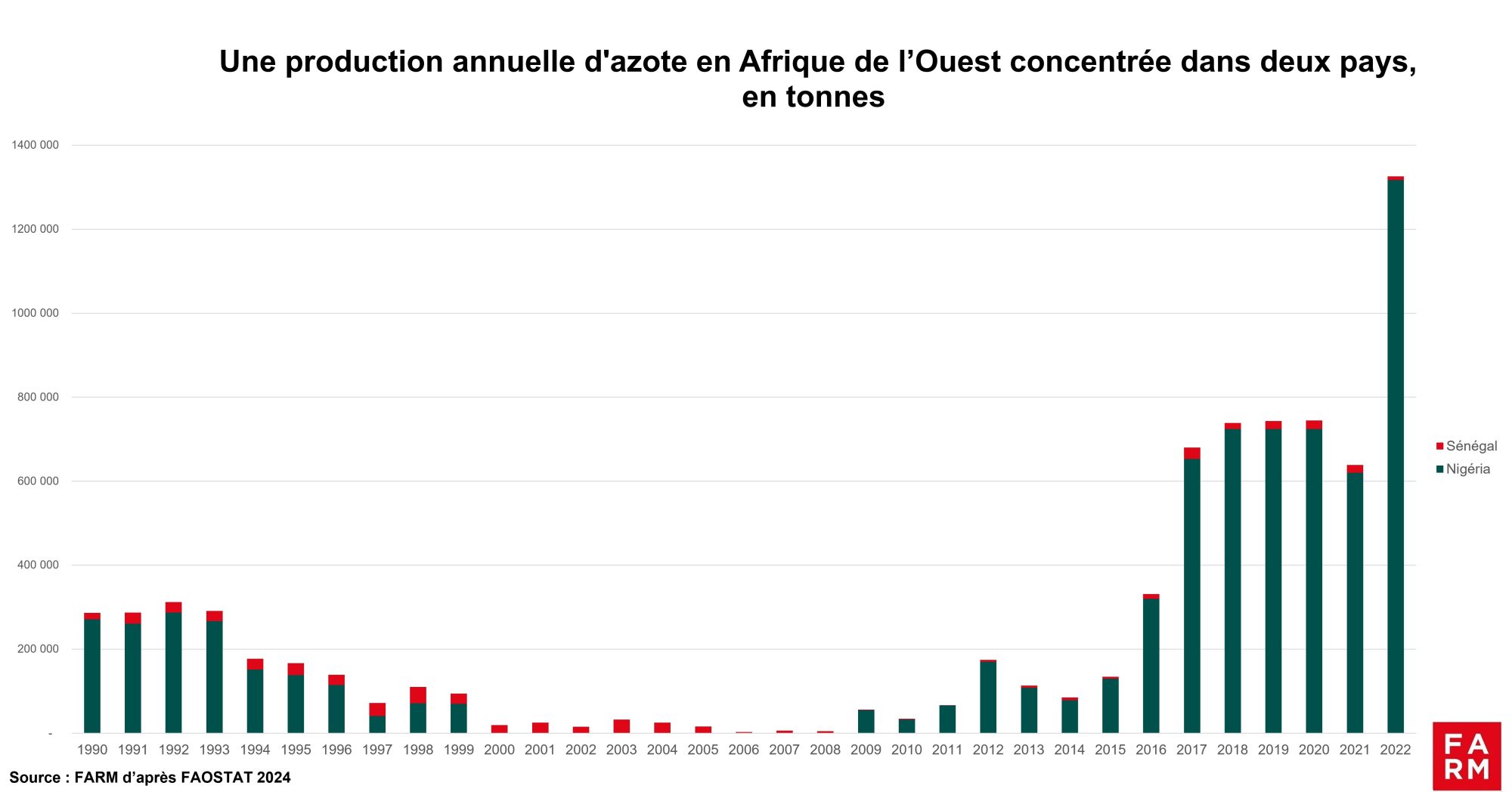

Nigeria, a future major player in the nitrogen market in a region where local production remains too low

Nitrogen production in West Africa, meanwhile, has been concentrated mainly around two players: Nigeria and Senegal. This situation has been marked by significant variations over time, revealing an uneven distribution of production capacity across the region. A surprising aspect of this dynamic is the apparent interruption of nitrogen production in Nigeria between 2000 and 2008. This period saw Senegal become the sole regional producer, although production remained relatively modest.

The lack of nitrogen production in Nigeria between 2000 and 2008 could be explained by several factors. First, the political and security situation in the Niger Delta had a significant impact on the hydrocarbon industry, which is closely linked to nitrogen production. Conflicts and attacks targeting energy infrastructure may have led to disruptions in energy production, also affecting fertilizer plants. In addition, governance and resource management issues may have also played a role. Nigeria has often faced challenges related to corruption and inefficient infrastructure management, which may have hampered the country's ability to maintain stable nitrogen production. Finally, fluctuations in the global fertilizer market and changes in agricultural policies may have limited nitrogen production during this period.

However, as the nitrogen production graph in Africa indicates, Nigeria has been developing an investment strategy since 2016 to increase its production capacity in order to become self-sufficient. To do this, Nigeria is using its gas reserves (4th world reserves) to produce ammonia, a key raw material for nitrogen fertilizers. With the Presidential Fertilizer Initiative launched by President Buhari, Nigeria also intended to influence the African continent and targeted the markets of other emerging countries with very high demand, such as Brazil and India. Thus, between 2019 and 2023, Nigerian production of urea (the solid nitrogen fertilizer that contains the most nitrogen) increased by 150 %. These strategies have notably made it possible to lower local fertilizer prices by 30 % over the period 2016-2021. The country has implemented a trade policy limiting imports of NPK blend to promote the local industry of blending (mixture of N, P and K fertilizers) while subsidizing and promoting partnerships with private investors such as the Moroccan group OCP. Despite these significant advances, challenges persist, particularly at the time of the war in Ukraine, with rising prices and the priority given to satisfying more profitable foreign markets. In addition, weaknesses in gas logistics and supply chains do not yet allow Nigerian production to fully expand.

Supply disruptions due to Russian aggression in Ukraine and long-term impacts to be expected

![]()

Global nitrogen fertilizer markets have been significantly disrupted in recent years, due to economic impacts of the 2008 crisis, the COVID-19 pandemic and the war in Ukraine. The price of a tonne of urea, the main source of nitrogen for agricultural use, has reached levels not seen since 2008, rising from 695 US$ at the end of October 2021 to nearly 925 US$ in April 2022. The Black Sea region and Russia in particular is a major exporter of urea but also of gas used for the production of fertilizers, particularly in Europe and India. The war in Ukraine immediately led to a reduction in the supply of Russian and Ukrainian nitrogen fertilizers on the markets, and, as a result, an increase in prices and price volatility, in line with that experienced after the lockdowns due to the COVID 19 pandemic. Since COVID 19 in 2020 and the Russian invasion of Ukraine in February 2022, the price per ton of urea has increased 4.5-fold, further disrupting access to nitrogen fertilizers for countries in the West African region. At the continental level, more than half of the countries import fertilizers from Russia and Ukraine, and in particular Benin and Nigeria which have dependency rates above 45 % according to Ousmane Badiane and Ali. West African countries are among the most dependent on the continent for imports of nitrogen fertilizers and potash from the Black Sea region (Russia, Belarus and Ukraine), as David Laborde points out. and Ali in their report for the CGIAR. Three combined factors may have disrupted the supply of nitrogen fertilizers to West African countries and likely restricted West African farmers' access to nitrogen fertilizers, which could have repercussions on agricultural productivity and food security in the region :

- Reduced supply: The interruption of Russian exports has limited the availability of nitrogen fertilizers on the international market

- Increased prices: The war has led to a surge in fertilizer prices on the world market, making it more difficult for African countries to purchase them.

- Logistical challenges: Disruptions in supply chains and shipping have complicated the delivery of fertilizers

Conclusion and major trends

Several major findings emerge from the recent analysis of the nitrogen fertilizer sector in West Africa, shedding light on both the structural challenges and the opportunities to be seized for food security and regional agricultural development:

A general intensification of nitrogen use in West African agriculture, linked to the context of population growth and the need to increase agricultural productivity, but the levels of use of nitrogen fertilizers still remain proportionally significantly lower than elsewhere in the world in a context of soil fertility crisis.

Increased dependence on imports, despite the increase in exports (which until the last period 2012-2022 were mainly destined for the West African market), which raises questions about food sovereignty and vulnerability to fluctuations in the global market.

A persistent concentration of production in a few countries, which creates regional disparities and challenges for nitrogen self-sufficiency.

An evolution of commercial relations, desired or suffered, depending on geopolitical impacts and the choices of fertilizer suppliers.

Strengthening intra-regional trade, although this remains relatively limited compared to trade with outside the region. Until 2011, intra-regional trade was more important than exports to third countries. Senegal and Ivory Coast are positioned as the leading re-exporters in the area.

Intraregional conflicts and political and financial instability have an impact on the production capacities of the main nitrogen-producing countries, which depend largely on the energy sector.

These observations support the need for West African countries to develop coordinated strategies to improve their nitrogen and nitrogen fertilizer production and reduce their dependence on imports. This is a crucial area for food security and agricultural development in this region which is facing a deterioration in soil quality and a decline in fertility as we recalled in a previous publication and which will also experience a doubling of its population by 2050.

This situation also constitutes an opportunity for the supplier countries of the sub-region, notably Nigeria, which through heavy investments in its industries Indorama, Notore and Dangote Group, could provide West Africa with losses from reduced nitrogen imports from Russia.

If you are interested in this topic, find FARM's analysis on phosphorus And potassium.