West African phosphates: developing production and anticipating health risks

Phosphorus, symbolized by “P” in the NPK formulation of mineral fertilizers, is essential for agricultural production, particularly for root development and plant maturation. It is mainly absorbed during vegetative growth and is involved in seed and fruit formation, making it a key element in optimizing agricultural yields and ensuring food security, both in West Africa and globally. FARM provides an initial analysis of the situation of phosphate trade flows between West Africa and the rest of the world.

Methodology

This analysis explores the evolution of average annual trade and consumption of phosphorus, expressed as pure mineral elements (P) for agricultural use between West Africa and seven major geographical areas over three decades (1990-2022). The data, taken from FAOSTAT (2024), are represented by maps illustrating three distinct periods: 1990-2000, 2001-2011 and 2012-2022. Imports are visualized by histograms, exports by arrows proportional to volumes and consumption by flat colors reflecting intensity.

West Africa, a minor player in the global phosphate market

The production of industrial phosphates and phosphate fertilizers involves several steps, from mining and preparation of phosphate rock to chemical transformation into phosphoric acid and fertilizer production. Once extracted, the phosphate rock is transported to processing sites. According to estimates, in 2021, more than 85 % of phosphoric acid obtained from the processing of phosphate rock was destined for the fertilizer industry.After enrichment, the phosphate ore is treated with sulfuric acid to produce phosphoric acid, which is used in synthetic fertilizers. The nature of the phosphate traded is important because once exported it may undergo processing that requires expensive infrastructure before it can be used by farmers.

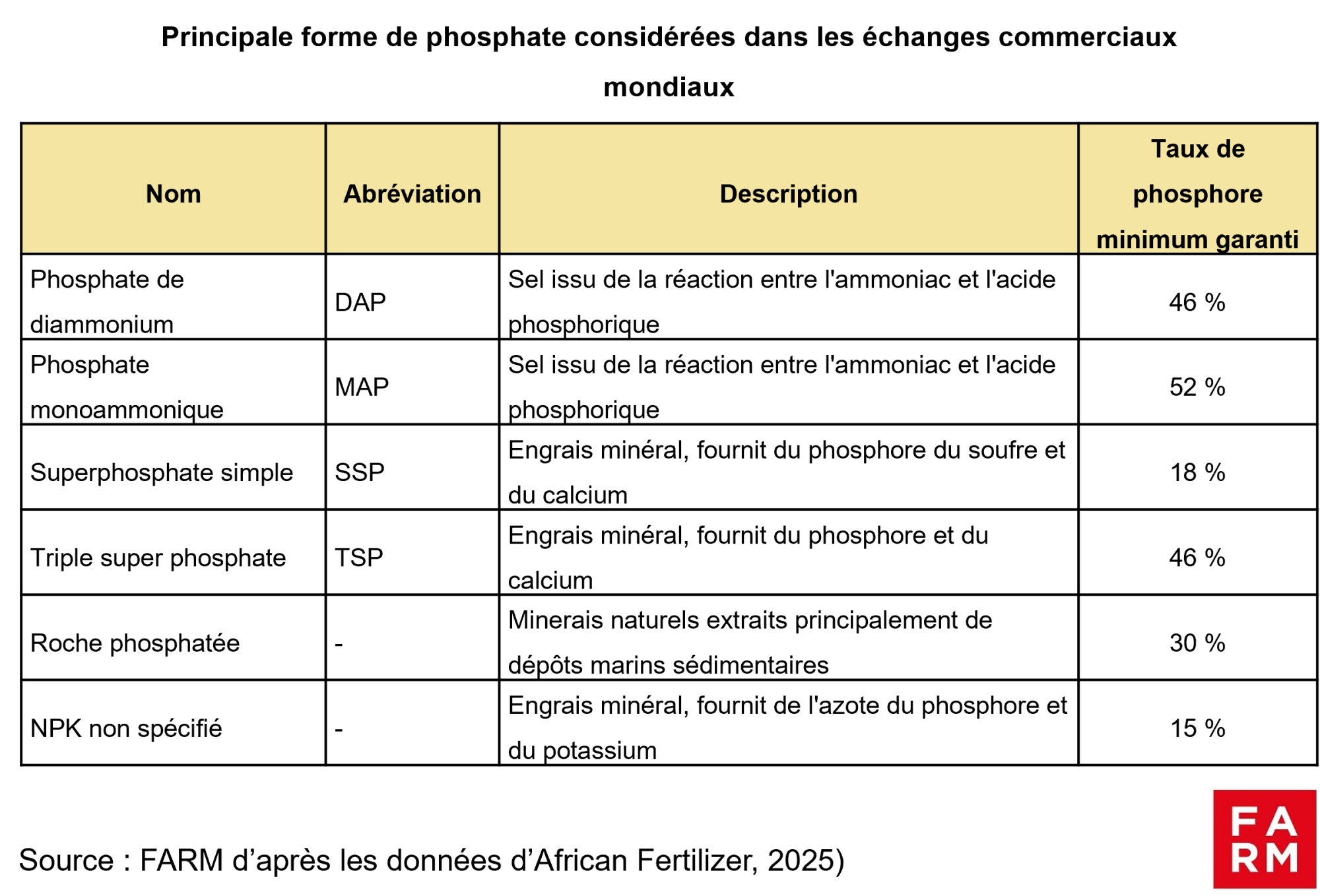

Phosphate trade takes place in different forms, mainly 6, with variable pure phosphorus levels:

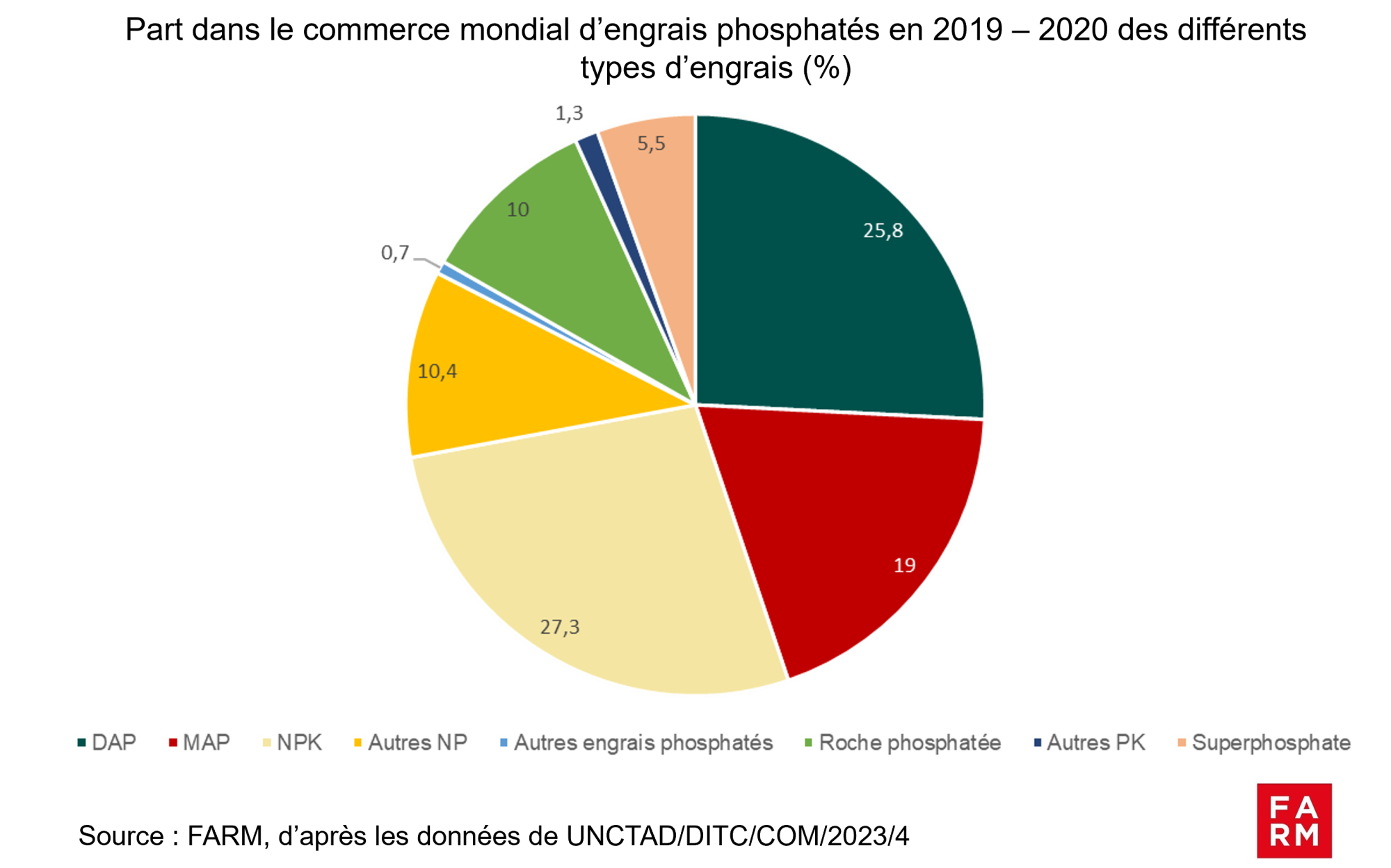

The main forms of phosphate fertilizers traded on the global market are DAP, MAP and NPK, which alone accounted for 72 % of global trade in 2019-2020.

Global phosphate fertilizer exports are dominated by a few large producers with abundant mineral resources and an efficient processing industry. China remains the leading exporting country, closely followed by Morocco and Russia. Brazil and India are major importers, with 14 and 12 billion tonnes of global phosphate fertilizer imports in 2019-2020, respectively. Both countries are also the leading importers of DAP and MAP. Overall, Asia-Pacific dominates global demand, with India, China, Bangladesh, and Vietnam, even though Brazil is by far the world's largest market. West Africa, for its part, accounted for only 1.3 billion tonnes of imports in 2022, compared to 0.58 billion tonnes of global consumption.

In West Africa, phosphate flows reflect varying trade strategies

Analysis of data from 1990 to 2022 shows a general increase in imports and exports in West Africa. However, production declined sharply, especially between 1990 and 2011. Consumption also declined during this period, from an annual average of 130,000 tonnes to 113,000 tonnes. However, over the last period, consumption increased, reaching an annual average of over 260,000 tonnes of phosphate.

In the 1990s, Nigeria produced phosphates, but on a small scale and mainly via phosphate nodule deposits. These deposits, often associated with uranium mineralization, never reached significant industrial exploitation (notably due to the difficulty of precisely identifying the country's real reserves). Unlike countries like Togo or Senegal, Nigeria has not developed a structured phosphate production sector, pushing it to turn to importing phosphates mainly from Europe over the period 2000-2011 and then from Morocco over the period 2012-2022.

Several strategies can be identified among the countries in the region. An export strategy, particularly for Senegal, which maintains high levels of exports to the Americas despite relatively low domestic consumption. A re-export strategy is evident in countries such as Mali, which import significant quantities of phosphates for subsequent re-export, thus acting as intraregional trading platforms. Furthermore, an agricultural development strategy is illustrated by the increase in consumption in countries such as Ghana and Côte d'Ivoire, which could reflect efforts to intensify agricultural production. A strategy of diversifying supply sources is also emerging, marked by a clear shift in the early 2000s, where Europe became a secondary partner to the benefit of the rest of Africa, and particularly Morocco.

These strategies depend on many factors, including logistical, regulatory and financialThe inadequacy of transport infrastructure, particularly maritime, necessary for the import of phosphate fertilizers, creates unequal access to the market depending on whether the country has access to the sea. In addition, divergent regulations between countries complicate coordination between States, particularly in the control of the quality of fertilizers.

Morocco and the OCP, phosphates (also) turned towards Africa

Since the mid-1980s, Morocco, which holds more than 70% of the world's phosphate rock reserves, has developed an ambitious strategy to increase its production and exports of phosphate fertilizers. In Morocco, the Jorf Lasfar site, launched in 1984, is now the world's leading phosphate fertilizer production platform. With investments made by the state-owned OCP (Office chérifien des phosphates) group, Morocco's market share of phosphate fertilizers has increased from less than 5 billion 300 tonnes in 2004-2005 to 15 billion 300 tonnes in 2019-2020. Although the Cherifian kingdom has the largest reserves, China remains the world's leading producer and exporter.

The development of Morocco's phosphate rock processing capacity to compete on the global market has not left the African continent on the sidelines. In 2000, the country became West Africa's leading partner for phosphate imports. In 2016, the group launched OCP Africa, a subsidiary dedicated to developing its activities on the African continent. This initiative aimed to increase the group's sales in Africa fivefold by 2025 (actually multiplied by 2 between 2018 and 2024 according to their financial reports). However, in West Africa, OCP has particularly intensified its efforts by implementing specific programs such as Agribooster, launched in 2015, which aims to create a ecosystem to facilitate producers' access to inputs, and seeks to establish partnerships with various West African countries: for example, in 2024, the group began discussions with Mali aimed at strengthen the use of fertilizers in the agricultural sector, Togo, for its part, signed an agreement in 2023 to build a phosphate fertilizer production plant and thus exploit its phosphate reserves. In 2019, the phosphate giant signed an agreement with Ghana for the construction (planned for 2026) of a phosphate fertilizer production plant with a production capacity of one million tonnes per year. In Nigeria, OCP inaugurated in 2022 a plant for the manufacture of phosphate fertilizers, importing phosphoric acid from Morocco and transforming abundant Nigerian gas into ammonia to manufacture MAP/DAP. OCP is positioning itself more generally as a major partner of West African countries in the agricultural sector, thus stimulating demand for fertilizers. This is evidenced, for example, the recent announcement the launch of a fund dedicated to the transformation of African agriculture, by Innovx, a subsidiary of the Mohamed VI Polytechnic University, founded and financed by the OCP group. Finally, to consolidate its position as a global leader and its presence in Africa, OCP plans to continue to invest massively in the years to come. A plan $14 billion investment is planned for the period 2025-2027.

Phosphate reserves in West Africa, but little exploited

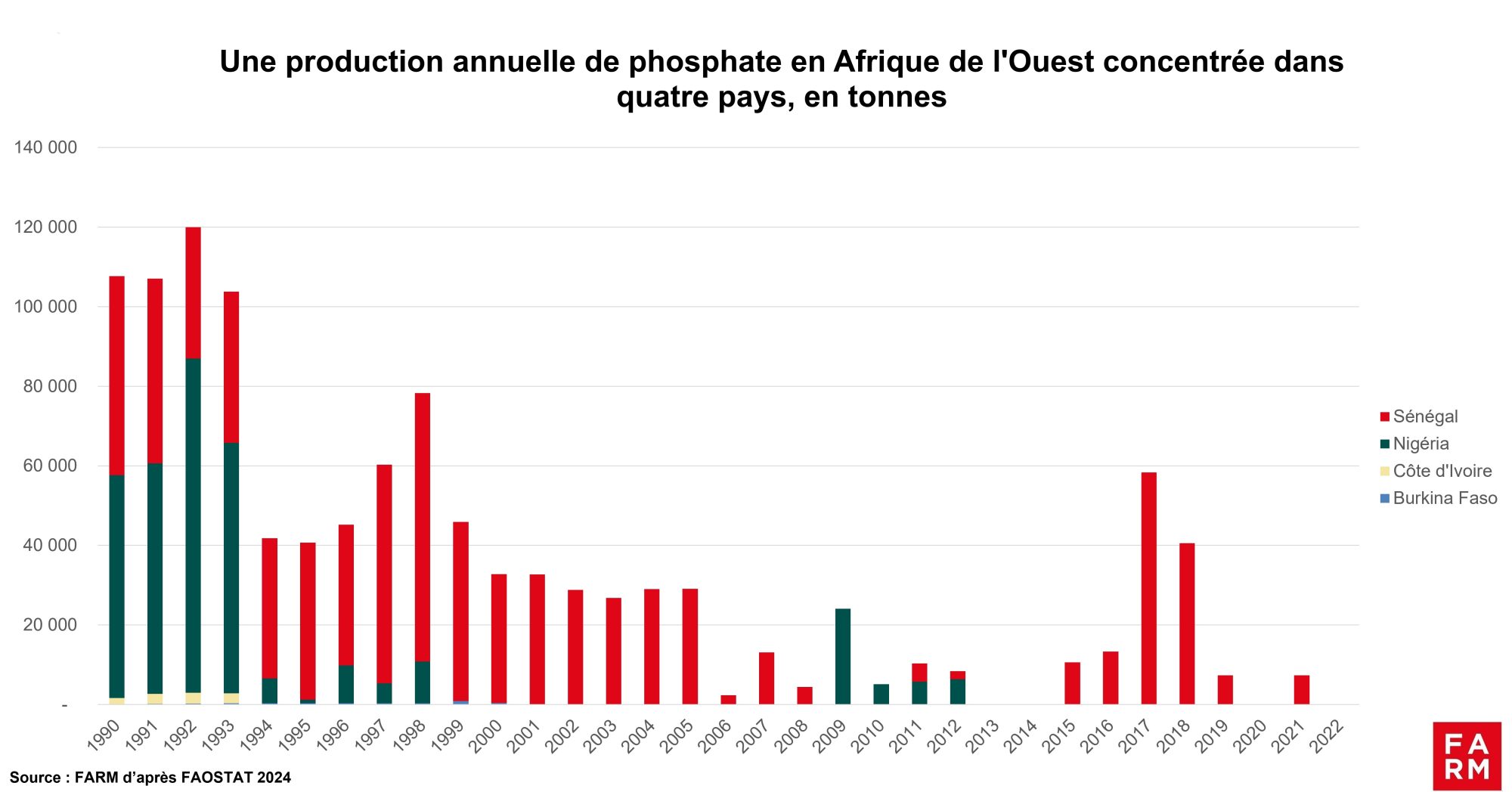

Analysis of phosphate production data in West Africa reveals several trends. Phosphate production has declined significantly in the region, despite a peak in 2017-2018 for Senegal at 60,000 tonnes. Total production has declined from 119,956 tonnes in 1992 to very low levels in recent years. In the early 1990s, four countries (Burkina Faso, Côte d'Ivoire, Nigeria, and Senegal) were producing phosphates. However, towards the end of the period studied, most ceased production. Production in each country shows significant fluctuations from one year to the next, highlighting instability in the sector, exacerbated by structural and geopolitical challenges.

There are several possible reasons for the decline in phosphate fertilizer production in the region. First, phosphate deposits may have been depleted or become economically unviable. Second, deteriorating market conditions, such as falling world phosphate prices or rising extraction costs, may make production unprofitable.Lack of investment in infrastructure Necessary for extraction and transportation can also hamper production. Political instability, including regime change or conflict, can also disrupt mining operations. Furthermore, increased international competition, with the emergence of more competitive producers on the global market, can marginalize these countries. Finally, policy changes, whether in government policies regarding mining or the environment, can affect production. The demand side, which faces economic and physical accessibility constraints and is not sufficiently stimulated by government policies or support, should not be underestimated.

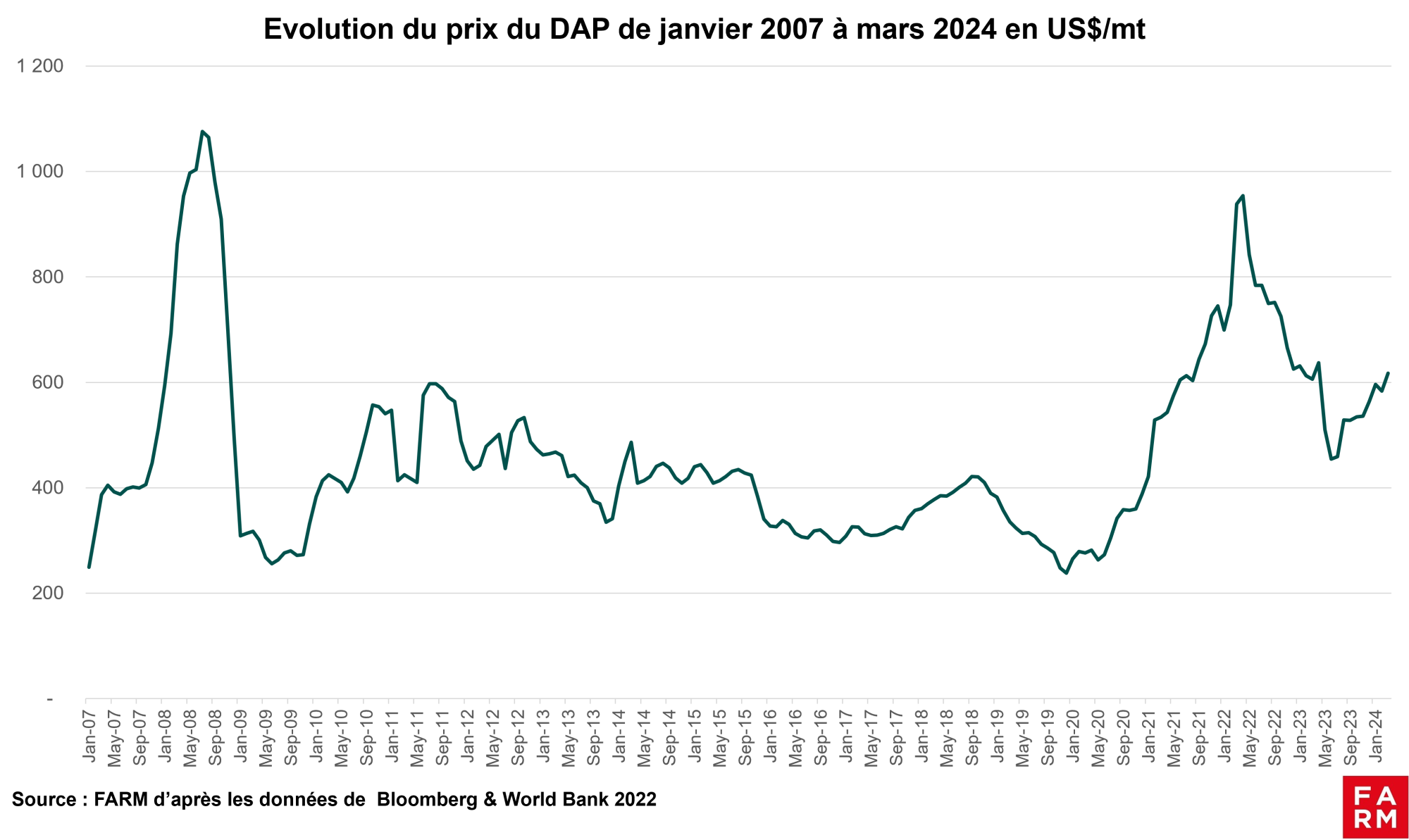

The main obstacle to the use of phosphate fertilizers in West Africa remains their high cost. Phosphate prices, particularly DAP (which represents more than 25 % of global trade), have increased significantly and experienced high volatility. They have been significantly impacted by the various crises of the last 15 years, thus exacerbating the difficulty of accessing phosphate fertilizers for countries and producers in the West African region. For example, during the agricultural price crisis in 2008, DAP prices increased 4.3-fold before falling and increasing again with the COVID-19 crisis and Russia's aggression against Ukraine, multiplying them again by 4 between 2019 and 2022.

Cadmium pollution from phosphates, a "health bomb" for West Africa?

The issue of cadmium levels in the human body and in soils has been the subject of renewed attention in the public debate in France in spring 2025 because of of its proven toxicityIn West African countries, studies and work also demonstrate a growing concern about the accumulation of heavy metals, including cadmium, in crops.

Apart from tobacco, which particularly concentrates this metal, food represents the main route of population exposure to cadmium, particularly through the consumption of cereals, vegetables, roots and tubers. In these plant foods, cadmium is absorbed from the soil, itself contaminated by deposits from atmospheric pollution and by certain agricultural practices, in particular the use of phosphate fertilizers. In France, they are responsible for 75 % cadmium inputs into soil.

Cadmium is a naturally occurring element in soils and phosphate rocks. Its concentration is generally higher in sedimentary deposits, which represent the majority of deposits (particularly in Morocco). Igneous rock deposits where phosphate is also found, such as those in Russia, contain significantly less.

Due to the high toxicity of cadmium, regulations have been implemented defining a maximum threshold for cadmium in soils. Within the European Union, the maximum threshold is set at 60 mg of cadmium (Cd) per kg of P₂O₅ in phosphate fertilizers, with a trend towards a gradual reduction towards 20 mg Cd/kg of P₂O₅. West African countries have a harmonized regulatory framework through the Economic Community of West African States (ECOWAS) which sets specific limits for heavy metals including cadmium (Regulation C/REG.13/12/12 and implementing regulation ECW/PEC/IR/02/03/2016). The maximum tolerated concentration of cadmium in fertilizers is expressed in ppm per 1% of P₂O₅, which makes direct comparison complex. According to our calculations, however, these thresholds appear significantly higher than those of the European Union, which can reach around 1,000 mg of Cd/kg of P₂O₅.

The risks of cadmium pollution can be aggravated by several factors:

The acidic nature of West African soils. West African soils generally exhibit a Acidic to weakly acidic pH, between 5 and 7. However, the Cadmium availability and mobility increase markedly when soil pH is acidic, following a decreasing logarithmic curve as the pH rises. Conversely, soils with neutral or alkaline pH favor the adsorption of cadmium on soil particles, which reduces its bioavailability to plants and limits its mobility in the environment.

There low organic matter content West African soils. Organic matter plays a key role in cadmium adsorptionThe richer a soil is in it, the more it limits the bioavailability of cadmium for plants, thus reducing the risks of pollution for the environment and human health.

Cadmium content of West African sedimentary deposits particularly those from Togo and Senegal, have particularly high cadmium levels compared to other global suppliers. Concentrations generally vary between 58 and 87 mg of cadmium per kilogram of P₂O₅.

Although the cadmium content of West African deposits is higher than that of Moroccan phosphates – which represent 58 % of regional consumption in 2022 according to the FAO – the quantities of fertilizers applied in the region remain relatively low. According to the FAO (2022), they are ten times lower than those observed in France, a country which has also reduced its consumption of phosphate fertilizers by 70 % since 1972These consumption levels currently limit the risk of exceeding agricultural thresholds, as highlighted by a recent study published in 2025 in the journal ScienceThese consumption levels should be considered as averages that do not take into account the heterogeneity of the volumes applied according to the sectors and territories. Nevertheless, these elements call for vigilance regarding the exploitation of Togolese and Senegalese deposits.

In the West African context, where soils are undergoing a progressive degradation and a decrease in their mineral content, abandoning phosphate fertilization would only accentuate the degradation and the decline in soil productivity. The supply of phosphates therefore remains essential, with regard to the nutrient balances of the soil, to compensate for this soil fertility deficit and ensure food security in the region while prioritizing the use of local resources in order to strengthen the region's food sovereignty. A key issue lies in the implementation of precautions and good practices when using phosphate fertilizers (see box below), rather than in questioning mineral fertilization itself.

Decadmiation consists of reducing the cadmium content of phosphate fertilizers by chemical treatments at a cost of approximately 100 US$ per tonne of P₂O5[1] If the exploitation of phosphate deposits in West Africa were to develop, the implementation of such processes would be recommended in order to limit their cadmium content as much as possible. Support through public-private partnerships with other industrialists such as OCP and West African national research centers would be necessary. OCP and European processing companies are already engaged in this process.

Phytoremediation is a technology that uses so-called “hyperaccumulator” plants to absorb heavy metalsThis process, although complex to implement in a context of land pressure, remains relevant if it is integrated into a more or less long-term crop rotation. Several plant species have proven their worth, particularly in French agricultural systems. We can cite Salix viminalis, Arabidopsis halleri or even Noccaea caerulescens. However, the question of the management of plant waste rich in cadmium arises, an issue which is still under development at present and which requires investment in treatment infrastructure.

Organic fertilization through the addition of compost, manure or plant residues, could contribute to trapping more cadmium, thus limiting its absorption by crops and reducing the risks of environmental and food pollution. This observation further confirms the importance of organo-mineral fertilization.

Reasoned and optimized mineral fertilization allows phosphorus inputs to be precisely adjusted according to the actual needs of crops and soils and to avoid over-fertilization. The use of biostimulants, which optimize the absorption of phosphorus fertilizers by the plant and make insoluble phosphorus from the soil bioavailable could also be favored.

Genetic improvement of varieties, which can follow two complementary axes: on the one hand, select or develop food crops which absorb less cadmium (especially rice); on the other hand, optimize intercalary species dedicated to phytoremediation so that they capture more cadmium in the soil.

[1] This represents a cost of €2 per hectare of wheat in France in 2014.

Conclusion

West Africa, although endowed with limited but not insignificant phosphate reserves, lacks the technical and financial means to fully exploit them. This situation leads to a dependence on phosphate imports, a product whose price is highly volatile and whose availability is threatened by international financial and geopolitical crises. This dependence makes the region vulnerable and threatens its agricultural sovereignty. However, it is essential to increase the supply of phosphates to West African soils, which are experiencing decreased fertility and decreased availability of essential mineralsThese contributions will be sustainable if they are also part of organo-mineral fertilization and an effective process for managing cadmium pollution.

By way of comparison, phosphate fertilizer consumption in Asia increased fivefold between 1970 and 2019, an increase correlated with the development of its agricultural production and productivity. This development, with all the limitations it implies in terms of the environmental impact of the Green Revolution, calls into question the trajectory of phosphate consumption that West Africa could experience. Furthermore, Asia has experienced a plateau in its phosphate consumption since 2012, perhaps suggesting a possible redirection of flows towards West Africa? Investments by Morocco and the OCP Group in its production capacity and in trade and industrial relations with West Africa could also offer an opportunity to strengthen the phosphate sector in the region.

If you are interested in this topic, find FARM's analysis on nitrogen And potassium.