We can (and must) stop the crisis in international markets

Prices are soaring on international markets, particularly for essential food products such as cereals and vegetable oils. A sharp increase in food insecurity and malnutrition is to be feared in many parts of the world. There are fears of urban riots and political unrest, as occurred in many countries during previous crises (in 2008 and 2011). What are the root causes of the crisis and how can it be stopped? Mechanisms exist that could also prevent or manage future crises.

A double-edged crisis

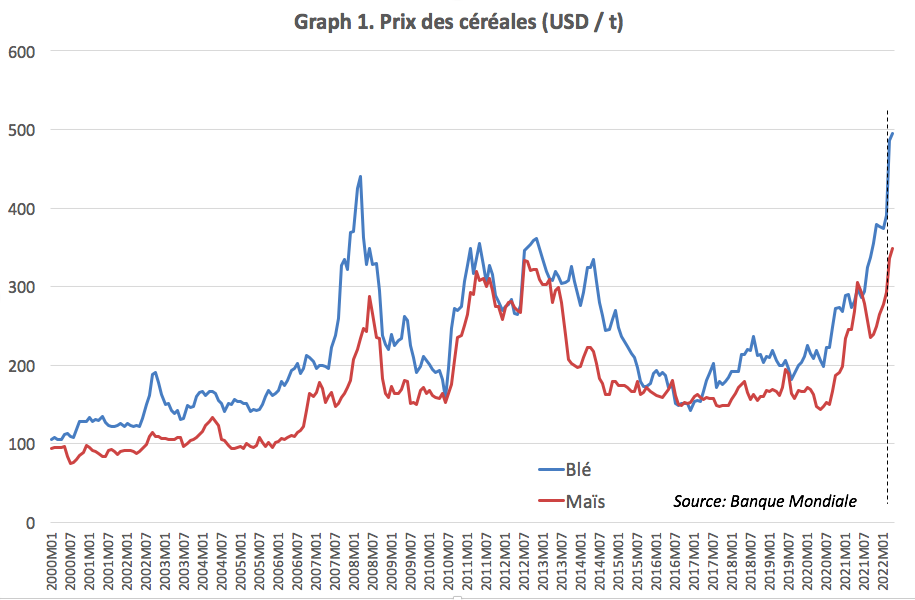

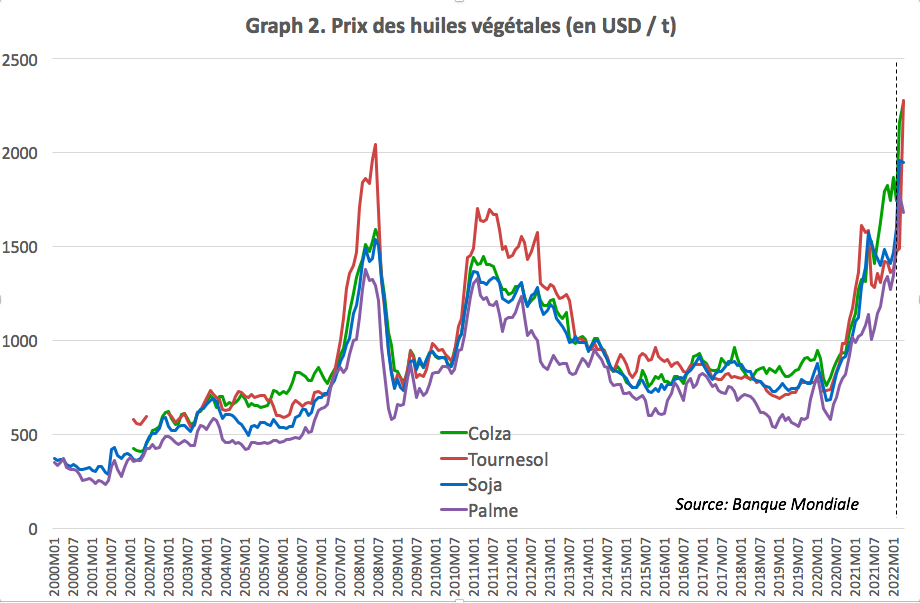

The first question is why. The answer seems obvious: the crisis is due to the war in Ukraine. However, it's more complicated. Because prices began to rise in mid-2020, as can be easily seen in Figures 1 and 2, where the dotted vertical line represents the start of the war in Ukraine. On the eve of the war, prices had already practically doubled.

Of course, the war in Ukraine hasn't helped matters. This region of the world (Ukraine + Russia) produces a significant share of the wheat and corn exported to international markets (around 20%), as does vegetable oils (especially sunflower) and nitrogen fertilizers. For the moment, it's not so much production that's compromised as exports (which traditionally went through the Black Sea ports).

But most of the price increase occurred before the war in Ukraine. And this is not a minor detail. Because if food prices, particularly those of corn, wheat, and vegetable oils, have risen sharply since mid-2020, it is because they have been driven up by the price of fossil fuels (oil and natural gas). What is at issue is our agricultural production model based on the intense use of these energies: chemical inputs (notably nitrogen fertilizers made with natural gas), mechanization, long-distance transport. What is at issue above all is our massive use of food products to produce fuel, especially in the United States (corn) and the European Union (rapeseed). This use strongly links the price of cereals (corn and wheat) and vegetable oils to the price of fossil fuels.

Of course, the war in Ukraine prolonged and amplified the crisis, but assigning it full responsibility is factually inaccurate. We (Europeans and North Americans) also have our (large) share of responsibility, and it is up to us to assume it.

We have the means to stop the crisis.

Stop the crisis

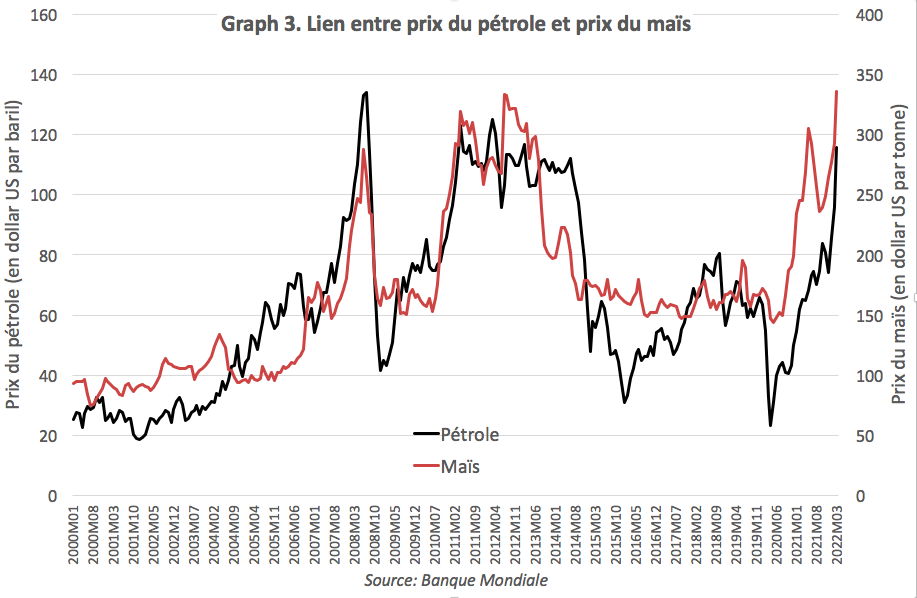

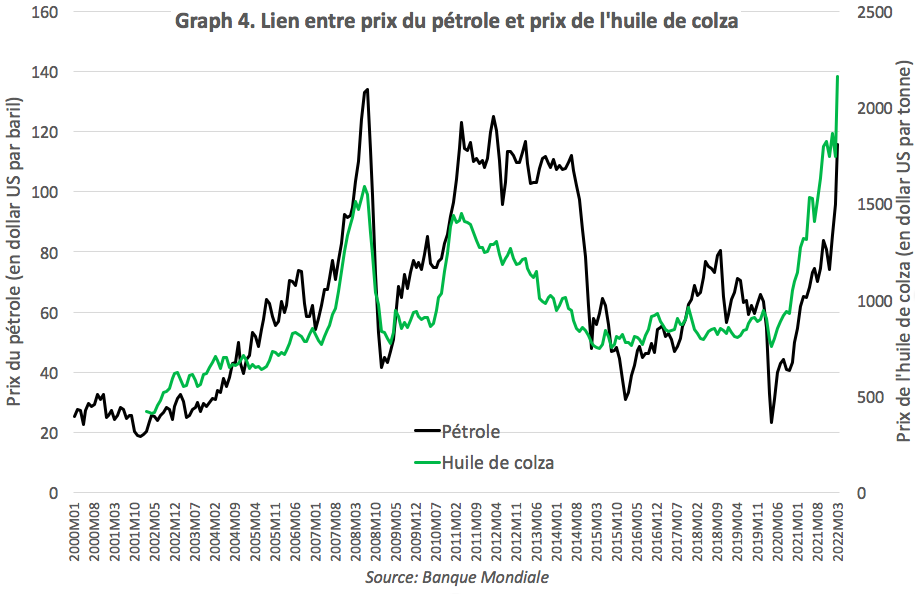

Because the main cause of the problem (agrofuels) could well turn out to be the solution. Graph 3 shows the link, very strong since 2008, between the price of oil and that of corn. This link is asymmetrical: when the price of oil increases, the price of corn increases, but when the price of oil falls, the price of corn only falls to a certain level from which it stabilizes (we observe a "floor").

This floor price is linked to biofuel support policies, particularly incorporation mandates that require the inclusion of a certain percentage of biofuels in fuel sold at the pump. As a result, massive quantities of corn are used to make fuel even when the price of oil is low enough to make this use unprofitable.

Reversing this mechanism would resolve the current crisis: it would be enough to ban (or at least cap) the use of grain to make fuel to bring international corn prices (and, by rebound effect, wheat prices) back to "reasonable" levels. The volumes involved are indeed considerable: in the United States, 140 million tons of corn are used annually to make fuel. For comparison, the "size" of the international corn market is around 200 million tons and that of the international wheat market is equivalent. And the wheat and corn exports potentially compromised by the Ukrainian conflict (wheat and corn exports from Russia and Ukraine) amount to around 85 million tons. Simply taking half of the corn usually used to make fuel would therefore erase the effect of the war in Ukraine.

This concerns cereals, and the United States. We in the European Union use little cereals to make fuel. On the other hand, we use enormous quantities of vegetable oils for this purpose (around 11 million tonnes, which represents 45 billion tonnes of the European Union's consumption). Our responsibility for the rise in cereal prices is small, but when it comes to vegetable oils, we are at the forefront.

Moreover, for vegetable oils, the mechanism is roughly the same as for cereals, with an asymmetrical link between oil prices and oil prices (see graph 4). And the proportions are also roughly the same: vegetable oil exports compromised by the Ukrainian conflict amount to 6 million tonnes, while in the European Union, 11 million tonnes of vegetable oils (mainly rapeseed oil) are used to make fuel. As with corn, taking half of this would cancel out the effects of the war in Ukraine.

We therefore find ourselves at a crossroads. Either continue to propose measures that we know will, at best, only slightly cushion the effects of the crisis (increasing food aid, asking countries not to restrict exports to the World Food Programme, asking countries to increase transparency about their stocks and policies, etc.). Or take responsibility by stopping this crisis that we helped create through our policies supporting agrofuels. We have the power and the duty to do so, but will we do it?

Preventing future crises

This crisis will not be the last to occur in international markets. So we might as well plan ahead.

Three mechanisms can be considered to prevent or manage future crises. The first involves perpetuating the mechanism proposed above to resolve the current crisis. It therefore concerns corn, wheat, and vegetable oils. The second mechanism concerns rice, a "separate" cereal, whose price is relatively disconnected from that of wheat and corn. This product is not affected by the current crisis, but it has experienced and will experience crises that will affect food security in Asia and also in parts of Africa and Latin America. It is not used to make fuel, but there is a "dormant" stock of rice that could be mobilized. The third mechanism is more generic and concerns WTO rules on public stocks.

Regulate the use of food products to make fuel. It would be enough to establish that when the international price of corn exceeds a predefined level, it is prohibited to use corn to make fuel. Or to provide for a gradual mechanism with different price thresholds triggering increasingly lower ceilings on the quantity of corn that can be used to make fuel. In short, it would be a matter of supplementing the current system (incorporation mandates) with a symmetrical system defining usage ceilings. Such a mechanism would be fully justified: since the current system offers protection to producers against price drops (the observed "floors"), it would be legitimate to ask them to accept a ceiling when prices soar. A similar mechanism could be put in place for vegetable oils. This would amount to considering the quantities of cereals or oils usually used to make fuel as "virtual stocks" that could be mobilized in a crisis situation, as was already proposed after the 2008 crisis.[1].

Transforming Japan's "WTO" rice stock into a virtual stock. When it joined the WTO, under pressure from the United States, Japan committed to importing the equivalent of 5 % of its rice consumption each year. This rice is imported and stored by the Japanese government (the population does not want it, it prefers locally produced rice). Some of it is given in the form of food aid (and ends up, for example, in the public stocks of Sahel countries), and some is used to feed livestock. But, of course, Japan does not have the right to re-export this rice that it was forced to import. In 2008, following the crisis on the international rice market, two experts - Tom Slayton and Peter Timmer - suggested that the United States government should exceptionally authorize the Japanese government to export all or part of its "WTO stockpile."[2]. This authorization was indeed granted and, without Japan having even exported a single grain of rice, the crisis ended on the rice market: the price of rice returned to acceptable levels. Indeed, anticipating a drop in prices, the countries that had blocked their exports removed the prohibitions and those desperate to import at any price decided to wait. A simple, effective and free solution (and one that would also suit Japan) would be to automate this process by stipulating that Japan will be immediately authorized to export its "WTO stock" as soon as the international price of rice reaches a predefined level.

Reform WTO rules on public stockpilesMany developing (or emerging) countries have public food security stocks. The state buys and stores cereals and distributes or sells them (sometimes at a subsidized price) when a food crisis occurs. The presence of such stocks plays an important role in the food security of the countries that use them, but it also contributes to the stability of international markets. Indeed, in the event of tensions on these markets (price increases, lengthening of import deadlines, shortages), importing countries tend to panic and import massively. This exacerbates the crisis on international markets. Thus, in 2008, it was estimated that 50% of the increase in the international price of rice was explained by these panic imports.[3]Having public stocks allows importing countries to avoid panic. However, WTO rules severely restrict the ability of countries to build up such stocks.[4]Since 2012, led by a group of 33 emerging and developing countries, negotiations have been underway to reform WTO rules in a way that gives countries more leeway to build up food security stocks. But these negotiations have still not been concluded, largely due to opposition from the United States and the European Union. Meanwhile, in 2019, China (under attack from the United States) was condemned for failing to meet its WTO commitments regarding its wheat and rice stockpiling policy. What will happen if, in the future, large countries like China or India have fewer stocks and turn more to international markets when they experience a poor harvest? Reforming WTO rules on public stocks seems more necessary than ever.

Essentially, the keys to these three mechanisms lie in the hands of the leaders of the United States and the European Union. Will they rise to the challenge?

[1] Wright, B., 2009. International Grain Reserves and Other Instruments to Address Volatility in Grain Markets. Policy Research Working Paper 5028, World Bank, Washington, DC.

[2] Slayton, T., Timmer, P. (2008). Japan, China and Thailand can solve the rice crisis—but US leadership is needed. CGD Notes (May), Washington, DC: Center for Global Development.

[3] Headey, D., 2011. Rethinking the Global Food Crisis: The Role of Trade Shocks. Food Policy 36, 136-146

[4] Galtier, F., 2017. Looking for a Permanent Solution on Public Stockholding Programs at the WTO: Getting the Right Metrics on the Support Provided. E15 Initiative. Geneva: International Center for Trade and Sustainable Development (ICTSD) and World Economic Forum. www.e15initiative.org/

2 commentaires sur “Nous pouvons (et devons) stopper la crise sur les marchés internationaux”

Leave a Reply

You must be logged in to post a comment.

Hello Franck,

I would like to add here that following the increase in food prices in 2020 due to the COVID-19 pandemic, the Sahel also experienced a very poor 2021-2022 agricultural season due to drought and other factors (floods, insecurity preventing access to the fields) which affected production in the western Sahel and even certain parts of the coastal countries.

In this regard, the war in Ukraine was a more significant phenomenon. This must be taken into account in your analysis. Otherwise, I fully agree with the recommended preventive measures.

Good evening Mrs. Dicko

Yes, you are right: the crisis on international markets has aggravated an already tense situation in the Sahel and West Africa. In particular, it has led to an increase in the price of oils and corn. Regarding corn, it seems that two factors played a role: i) the shortage of fertilizers in cotton-growing areas (which affected cotton production but also corn) and ii) demand from poultry farms in certain coastal countries (these farms generally buy imported corn, but given the rise in prices on the international market, they have turned to local corn).

In Mali, has the price increase spread to millet and sorghum? Has the price of fuel increased?